Airbus is looking forward to, and at the same time dreading, some upcoming changes in its operations and markets in 2019. A new CEO is taking the helm, and it remains an open question just how hard an impact Brexit will have on the firm.

First the good news. The market for large commercial transports continues to rise following a brief downtick in 2015-2016. Airbus set a new all-time order backlog record in 2018, boasting 7,577 jets on its books (of which 6,536, or 86%, are A220 and A320ceo/neo family narrowbodies). The number of Airbus aircraft to be built and delivered represents 9.5 years of shipments at the 2018 production level (see the Airbus/Boeing year-end 2018 report for more details).

Much of Airbus’ success can be attributed to narrowbody airliners such as the A320neo and its most recent addition, the A220. Designed by Bombardier, the A220 was formerly known as the CSeries but has been rebranded now that it is under the auspices of an Airbus/Bombardier joint venture. Adding the CSeries to its product line has cost Airbus little in sales and expands the company’s offerings down into the 100-130-seat range of the regional jet market.

The focus of late is on sharply managing aircraft delivery. Despite the difficulty in managing the supply chain, Airbus ramped up its delivery total to 800 aircraft in 2018, compared to 718 in 2017. Continued attention will be critical as Airbus has announced production rate increases on several models, including an unprecedented 60+ A320s per month in 2019. As such, the pressure on supply chains to meet the demands of delivering highly engineered components in increasing quantities and on just-in-time schedules will continue to be intense.

The fate of Airbus’ flagship A380 was sealed in early 2019 when its key customer, Emirates, canceled 39 of its remaining orders. The airline has opted to take delivery of only 14 more A380s over the next two years and will instead order 40 A330-900 and 30 A350-900 twin-engine widebody airliners. With no substantial A380 backlog remaining, production of the aircraft will end in 2021.

Airbus executives had resisted letting the program die given the prestige they attach to building the world’s biggest passenger jet. However, Airbus management is currently in flux. Airbus CEO Tom Enders is scheduled to depart in a couple of months; and with Emirates canceling so many orders, it made sense to kill the program before new management takes the helm.

Former Airbus Commercial Aircraft president Guillaume Faury has been selected to lead Airbus as its next CEO. He will hit the ground running as he deals with the potential fallout from Brexit. Brexit, which is set to occur in 2019 with the scheduled departure of the U.K. from the European Union, could hit the transnational factories of Airbus hard if no deal is reached.

Airbus’ wing production plant is located in the U.K. The operations there have been stockpiling parts in preparation for supply interruptions should a worst outcome Brexit occur. Should this happen, production delays will ripple through Airbus’ supply chain at a time when it needs to maintain a fierce level of manufacturing to fill its backlog. Even worse would be if the U.K. is no longer part of the EU’s aviation safety agency. In this scenario, Airbus would need to quickly shift production out of the U.K. to operations elsewhere in the European Union, the U.S., or China. Even in a best case, Airbus fears that additional costs in the U.K. will make it very difficult to make future investment in the region.

In military markets, Airbus Defence and Space reached a crucial agreement on its troubled A400M military airlifter with the program’s founding countries to delay deliveries and, most critically, revise financial penalties. Most recently, the company took a EUR2.2 billion charge on the program in 2016 due to gearbox issues, which affected deliveries and led partner nations to withhold payments. As a result of the agreement, the A400M production rate will gradually fall from 15 aircraft in 2018 to 11 in 2019 and eight from 2020 onward. This extension will give Airbus more breathing room to secure export sales, which have been slow in coming for the model.

The company, along with partner Dassault Aviation, will be a key contractor on Europe’s proposed Future Combat Air System (FCAS), which is slated to complement and eventually replace current- generation Eurofighter and Rafale fighter aircraft between 2035 and 2040. The program took a step forward in early 2019 when France and Germany let an equally financed EUR65 million two-year contract to begin development. Engine development for the FCAS is underway at Safran and MTU Aeroengines. The program will no doubt face years of painful politicking, but fears of a resurgent Russia may be enough of an impetus to keep it moving along.

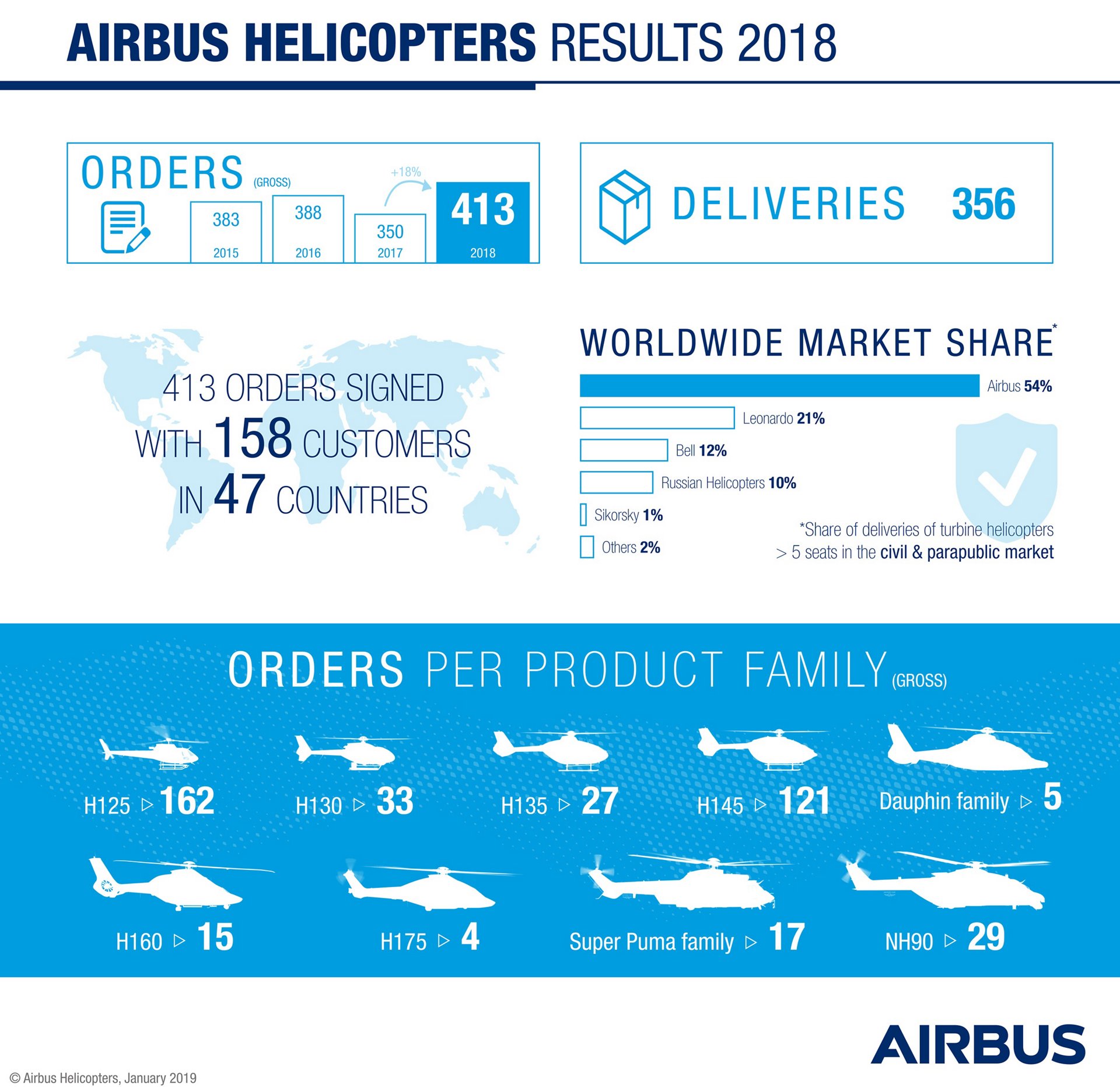

Meanwhile, Airbus Helicopters is improving its operations and continuing to grow its international presence. Airbus Helicopters delivered 356 rotorcraft and logged gross orders for 413 helicopters (net: 381) in 2018, with a strong commercial performance on the heavy and super-medium segments. Of that total, 148 orders were for light twin-engine helicopters of the H135/H145 family and another 15 orders were for the next-generation H160. At the end of 2017, the overall backlog stood at 717 helicopters.

In the U.S., Airbus Helicopters continues to reap the benefits of its 2006 selection for the U.S. Army’s Light Utility Helicopter requirement. The company’s UH-72A fulfills the Army’s LUH need, with a potential program life-cycle value of more than $2 billion. The decision marked Airbus’ first major win as a prime contractor for the U.S. military. Current plans call for the Army’s overall UH-72A acquisition to total 475 helicopters, production of which will run through 2020.

The company is hoping it can repeat this performance in the U.S. Army Future Attack Reconnaissance Aircraft (FARA) competition to replace OH-58D scout helicopters. Competition will be fierce, and the current political environment in the U.S. will likely put Airbus Helicopters in the underdog position versus Bell and Sikorsky.

Overall, Airbus is dealing with pending uncertainties as best as it can. The majority of the company’s programs are stable, which will ensure continued long-term success despite today’s difficulties.

A military history enthusiast, Richard began his career at Forecast International as editor of the World Weapons Weekly newsletter. As the Internet became central to defense research, he helped design the company’s Forecast Intelligence Center and now coordinates the FI Market Recap newsletters for clients. He also manages two blogs: Defense & Security Monitor, which covers defense systems and international security issues, and Flight Plan, focused on commercial aviation and space systems.

For more than 30 years, Richard has authored Defense & Aerospace Companies, Volume I (North America) and Volume II (International), providing detailed data on major aerospace and defense contractors. He also edits the International Contractors service, a database tracking all companies involved in programs covered by the FI library. Richard currently serves as Manager of the Information Services Group (ISG), which develops outbound content for both Forecast International and Military Periscope.

{kind=link}