COVID-19 Emerges as Potent Threat to Air Travel and Demand for Commercial Jets

by J. Kasper Oestergaard, European Correspondent, Forecast International.

While it would be premature to make detailed conclusions about how COVID-19 will impact the aviation industry in the future, even if the outbreak is short-lived, it is reasonable to argue that a major risk factor has emerged to air travel and aerospace manufacturing. While outbreaks of infectious disease across borders are not unprecedented, in recent history the impact has been geographically concentrated. The SARS outbreak in 2002-04 mainly impacted Southeast Asia and the 2013-16 outbreak of Ebola was predominantly in three nations in West Africa. COVID-19, while less lethal, has demonstrated that infectious diseases can fairly quickly cause great harm to worldwide economic activity due to the measures that need to be taken to contain it. While the aviation industry, and the air transport industry in particular, will not have to completely alter its approach to risk management, companies will certainly have to revisit and revise their models.

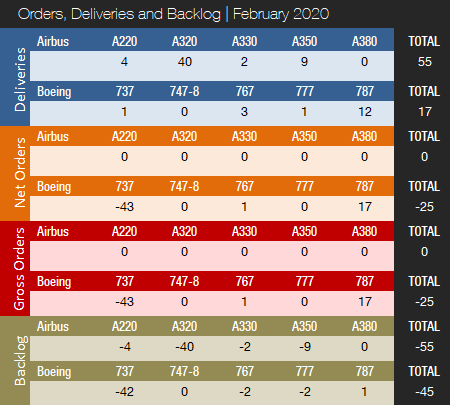

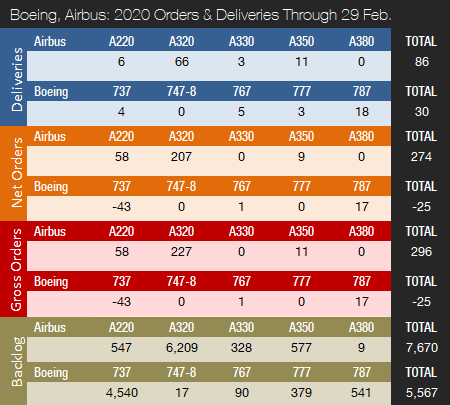

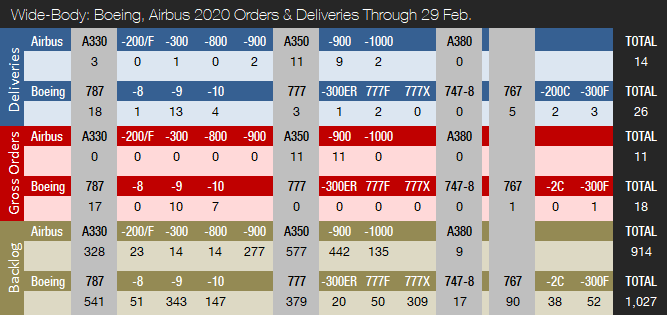

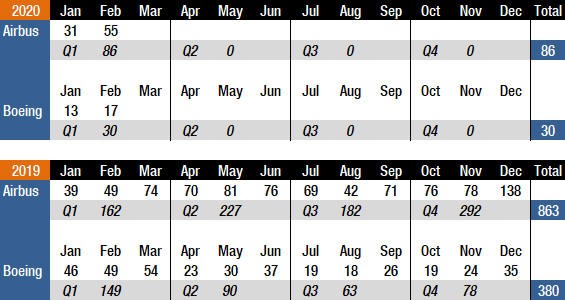

Turning to the February numbers for orders and deliveries, Boeing and Airbus delivered 17 and 55 commercial jets in February 2020 compared to 49 deliveries each in the same month last year. Boeing’s deliveries continue to suffer in the aftermath of two 737 MAX crashes and the subsequent deliveries halt and grounding of the fleet. Deliveries of 737 MAX aircraft have been suspended since March 2019. Year-to-date, Boeing has delivered 30 aircraft and is 65 deliveries behind last year’s total for the first two months of the year. Airbus delivered a total of 86 jets in January and February, compared to 88 in the same period last year. For the full year 2019, Boeing delivered 380 aircraft, while Airbus set a new all-time annual record, handing over 863 jets. Prior to this, Boeing had retained a deliveries lead over Airbus since 2012. In 2018, Boeing delivered 806 jets (763 in 2017), with Airbus handing over 800 (718 in 2017).

In December 2019, Boeing announced its decision to temporarily suspend 737 MAX production from January 2020. Prior to this, Boeing had been producing 737 MAX jets at a reduced rate of 42 aircraft per month and thereby built up an inventory of aircraft ready to be shipped. As of mid-March, the suspension is still in effect; however, Boeing expects the aircraft will resume service in mid-2020. In the meantime, test flights and software changes continue. Boeing has carried out more than 1,100 test flights with new MCAS software for a total of 2,100 flight hours. On January 10, the FAA announced that it remains focused on following a thorough process for returning the 737 MAX to service. The FAA continues to work with other international aviation safety regulators to review the proposed changes to the aircraft. The FAA made it clear that its first priority is safety and that no timeframe for when the work will be completed has been set. While Boeing is currently estimating that the grounding of the 737 MAX will be lifted during mid-2020, it will be a few years before the company is able to hit the planned monthly production rate of 57 aircraft. On January 30, Spirit AeroSystems, the 737 MAX fuselage manufacturer, announced that it had reached an agreement with Boeing for a restart of production and slow ramp-up of deliveries throughout the year to reach a delivery total of 216 737 MAX shipsets in 2020. To date, Boeing has delivered 387 737 MAX jets, of which 256 were delivered in 2018, up from 74 in 2017.

In February, Boeing delivered one 737NG, three 767s, one 777 and 12 787s. Boeing raised the monthly Dreamliner production rate to 14 aircraft during 2019 and handed over 158 787s last year – a new annual record. The company delivered 145 787s in 2018, up from 136 in 2017. The 787 production rate will be reduced from 14 to 12 aircraft per month in late 2020 and is expected to be further adjusted to 10 per month in early 2021, with a return to 12 per month in 2023. The 777 program awaits the 777X’s service entry. The first flight of the 777X was completed on January 25 and first delivery is targeted for 2021.

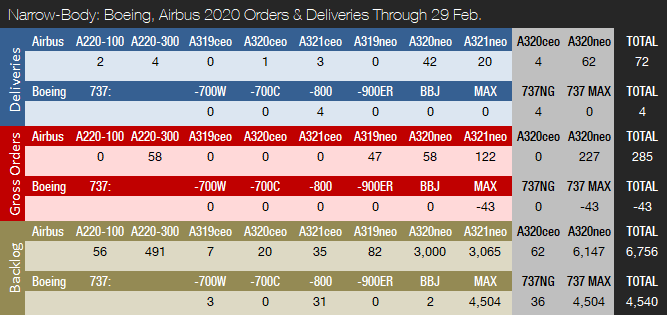

In February, Airbus delivered four A220s, 40 A320s (3 CEO / 37 NEO), two A330s, and nine A350s. Airbus increased the official A320 production rate to 60 aircraft per month during 2019 and is targeting an additional raise to 63 jets per month from 2021. Airbus is also discussing a further ramp-up with its supply chain and considers increasing the rate by one or two in 2022 and the same in 2023. This could bring the A320 production rate up to as high as 67 aircraft per month by 2023, equal to 804 jets per year, putting the company within reach of the 1,000-jets-per-year delivery mark. For the full year 2019, Airbus handed over 642 A320 family aircraft, of which 551 were A320neos. This compares to a total of 386 A320neo family aircraft delivered in 2018, up from 181 and 68 in 2017 and 2016, respectively. Airbus delivered a record 112 A350s in 2019, up from 93 and 78 in 2018 and 2017, respectively. Airbus increased the monthly A350 production rate to 10 during 2019. Airbus has been considering a further increase up to 13 A350s per month, but for 2020 the A350 is expected to stay at a monthly rate of 9-10 aircraft. Airbus expects to deliver 40 A330 jets in 2020, down from 53 in 2019.

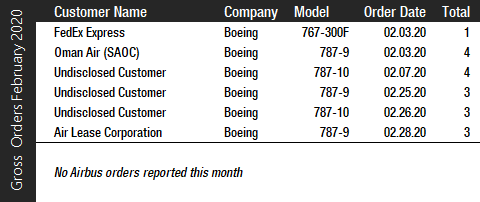

Turning to the orders race, Boeing reported 18 gross orders in February and 43 737 MAX cancellations, for a total of 25 net cancellations. Orders were mainly small 787-9 and -10 orders from multiple customers. Also, FedEx ordered a single 767 freighter. For the full year 2019, Boeing accumulated 243 gross orders (330 cancellations => -87 net new orders). For the full year 2018, Boeing booked 893 net new orders and 1,008 gross orders.

In February, Airbus reported no new orders or cancellations.

At the end of February, Airbus’ reported a backlog of 7,670 jets, of which 6,756, or 88 percent, were A220 and A320ceo/neo family narrowbodies. This is 55 aircraft below the company’s all-time backlog record of 7,725 aircraft set in January 2020. By the end of February 2020, Boeing’s backlog (total unfilled orders before ASC 606 adjustment) was 5,567 aircraft, of which 4,540, or 82 percent, were 737 NG/MAX narrowbody jets. Boeing’s all-time backlog high of 5,964 aircraft was set in August 2018. The number of Airbus aircraft to be built and delivered represents 8.9 years of shipments at the 2019 production level. In comparison, Boeing’s backlog would “only” last 6.9 years at the 2018 level, which we use as proxy for 2019 due to the drop in 737 MAX deliveries. This year to date, Boeing’s book-to-bill ratio, calculated as net new orders divided by deliveries, is negative due to cancellations exceeding gross orders. Airbus’ book-to-bill ratio is 3.19 thanks to very strong bookings in January. In 2019, Boeing’s book-to-bill ratio was negative, while Airbus reported a book-to-bill of 0.89.

2020 Forecast

Forecast International’s Platinum Forecast System® is a breakthrough in forecasting technology. Among many other features, Platinum provides 15-year production forecasts. The author has used the Platinum Forecast System to retrieve the latest delivery forecasts and, for 2020, Forecast International’s analysts expect Boeing and Airbus to deliver 491 and 858 commercial jets, respectively.

On January 29, in connection with the release of its 2019 earnings report, Boeing, as expected, did not provide a delivery target for the year due to the 737 MAX uncertainty. On February 13, Airbus reported 2019 earnings and announced a target of 880 commercial aircraft deliveries in 2020, up 2 percent from 863 in 2019.

Note: Boeing 777-300ER orders include one 777-200LR. The 777-300ER backlog includes two 777-200LRs.

Joakim Kasper Oestergaard is Forecast International’s AeroWeb and PowerWeb Webmaster and European Editor. In 2008, he came up with the idea for what would eventually evolve into AeroWeb. Mr. Oestergaard is an expert in aerospace & defense market intelligence, fuel efficiency in civil aviation, defense spending and defense programs. He has an affiliation with Terma Aerostructures A/S in Denmark – a leading manufacturer of composite and metal aerostructures for the F-35 Lightning II. Mr. Oestergaard has a Master’s Degree in Finance and International Business from the Aarhus School of Business – Aarhus University in Denmark.

References:

- http://www.boeing.com/commercial/#/orders-deliveries

- https://www.airbus.com/aircraft/market/orders-deliveries.html

- https://www.faa.gov/news/updates/?newsId=93206

- https://www.boeing.com/commercial/737max/737-max-update.page

- https://boeing.mediaroom.com/2020-01-21-Boeing-Statement-on-737-MAX-Return-to-Service

- https://boeing.mediaroom.com/2019-12-16-Boeing-Statement-Regarding-737-MAX-Production

- https://boeing.mediaroom.com/2020-01-29-Boeing-Reports-Fourth-Quarter-Results

- https://www.reuters.com/article/us-boeing-737max/boeing-unlikely-to-hit-pre-grounding-output-targets-for-737-max-before-2022-idUSKBN206291?il=0

- https://www.spiritaero.com/release/137055/spirit-aerosystems-announces-737-max-production-agreement-with-boeing/

- https://www.airbus.com/newsroom/press-releases/en/2020/02/airbus-reports-full-year-2019-results.html

A military history enthusiast, Richard began his career at Forecast International as editor of the World Weapons Weekly newsletter. As the Internet became central to defense research, he helped design the company’s Forecast Intelligence Center and now coordinates the FI Market Recap newsletters for clients. He also manages two blogs: Defense & Security Monitor, which covers defense systems and international security issues, and Flight Plan, focused on commercial aviation and space systems.

For more than 30 years, Richard has authored Defense & Aerospace Companies, Volume I (North America) and Volume II (International), providing detailed data on major aerospace and defense contractors. He also edits the International Contractors service, a database tracking all companies involved in programs covered by the FI library. Richard currently serves as Manager of the Information Services Group (ISG), which develops outbound content for both Forecast International and Military Periscope.