Formed at the start of the historic COVID-19 pandemic, the new Raytheon Technologies is doing as well as can be expected.

The merger of Raytheon and United Technologies Corp (UTC) in April created a $74 billion defense giant in the process.

The new Raytheon Technologies is now second in terms of defense contractors, behind Lockheed Martin. Overall, the company will be the world’s second largest aerospace and defense conglomerate after Boeing, with revenue roughly split between the two markets.

This “merger of equals” blends Raytheon’s defense expertise with UTC’s commercial aerospace operations. Because there is little overlap in the two companies’ product lines, the new Raytheon Technologies Corporation will be a diversified aerospace and defense conglomerate with products that range from missile defense systems to airline seats.

Raytheon Technologies reported second-quarter 2020 sales of $14.1 billion and adjusted sales of $14.3 billion. The company recorded a net loss from continuing operations in the second quarter of $3.8 billion and included $4.4 billion of net significant and/or nonrecurring charges and acquisition accounting adjustments. Adjusted net income was $598 million.

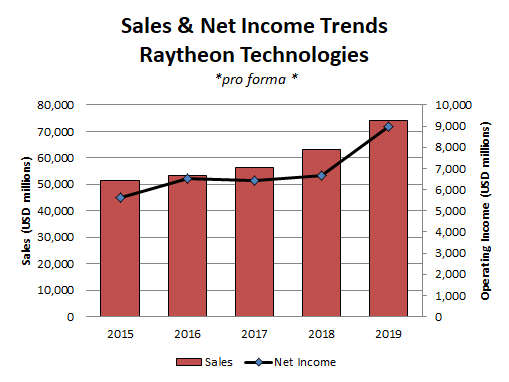

An unofficial, pro forma chart combining Raytheon’s and UTC’s results for the past five years is presented below.

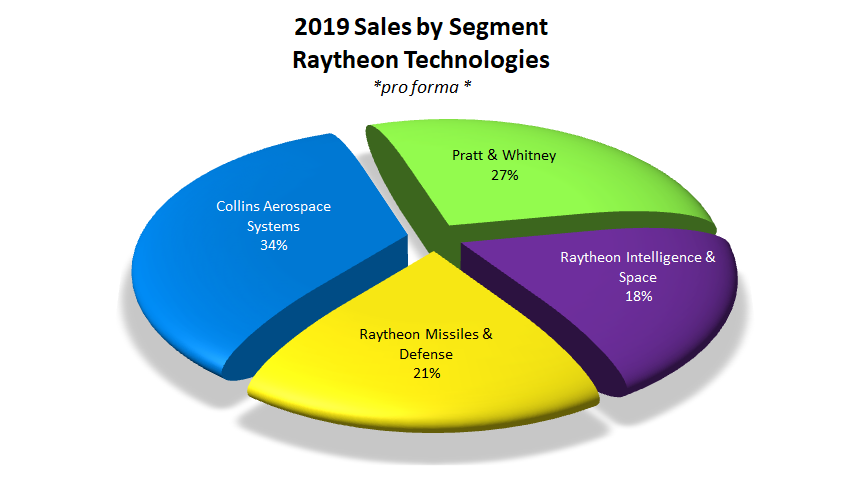

Raytheon Technologies consists of four businesses – the defense-oriented Intelligence, Space & Airborne Systems and Integrated Defense & Missile Systems, and the commercial aerospace facing Collins Aerospace and Pratt & Whitney.

This diversification has proven key to the company’s success in weathering the pandemic thus far. While the pandemic continues to deeply impact Raytheon Technologies’ commercial aero business, primarily Collins Aerospace and Pratt & Whitney, this is balanced out by Raytheon’s defense operations. This diversification should allow the firm to offset near-term commercial aerospace headwinds.

However, the pandemic has not left the company unscathed. The firm has slashed some 8,000 jobs in the commercial aerospace operations as a result of the dramatic drop in air travel. The cuts are part of an overall plan to shave some $2 billion in costs as the company seeks to preserve cash. The pressure on commercial aviation is expected to continue, with air traffic not likely to return to pre-pandemic levels until 2023 at the earliest.

While commercial operations suffer during the pandemic, the company’s defense business is so far putting in strong results. The company was awarded some major contracts in the first half of the year such as the new USAF long-range standoff weapon (LRSO), which is forecast to be worth some $10 billion over its lifetime. The defense unit also booked a $2.3 billion award for TPY-2 radars for the Kingdom of Saudi Arabia. These new wins, coupled with ongoing efforts, pushed the defense backlog to a record $73.1 billion – enough to provide a solid foundation for Raytheon Technologies over the next several years and beyond.

Looking ahead, the merged firm should be able to show its worth. Integration of assets is ongoing, and the company hopes to deliver over $1 billion in savings once it hits its “synergy targets.” This will likely be crucial, as many firms post-crisis will be squeezing to lower costs, in both commercial and military markets.

Industry primes such as Airbus and Boeing will be even more fervent in cutting costs, actions that originally pushed UTC to acquire Rockwell Collins and form Collins Aerospace.

At the same time, cost pressure is a notable constant in contracting with the Pentagon. By combining operations, the new company is looking to gain efficiencies of scale in its own operations to meet lower cost targets. Further, the diversification follows the old conglomerate model upon which UTC was based – when one market is down, the other is up, providing resiliency across business cycles – an axiom that is being strongly tested of late.

The next few years will be rocky as the industry copes with what is looking to be a lengthy crisis. Longer term, Raytheon Technologies is laying the groundwork to be strongly positioned once a “new normal” is established.

Forecast International’s Defense & Aerospace Companies, Volume I – North America service includes coverage of over 100 key U.S. and Canadian primes and their subsidiaries. Each of the 35+ reports contains data on recent programs, mergers, and joint ventures. Among the notable corporations covered are OEMs such as Boeing, Lockheed Martin, Raytheon Technologies, and General Dynamics. Also featured are Tier I and Tier II contractors and subsidiaries such as Pratt & Whitney, Honeywell, Parker Hannifin, and Spirit AeroSystems. Pricing begins at $2,295, with discounted full-library subscriptions available. Click here to learn more.

A military history enthusiast, Richard began his career at Forecast International as editor of the World Weapons Weekly newsletter. As the Internet became central to defense research, he helped design the company’s Forecast Intelligence Center and now coordinates the FI Market Recap newsletters for clients. He also manages two blogs: Defense & Security Monitor, which covers defense systems and international security issues, and Flight Plan, focused on commercial aviation and space systems.

For more than 30 years, Richard has authored Defense & Aerospace Companies, Volume I (North America) and Volume II (International), providing detailed data on major aerospace and defense contractors. He also edits the International Contractors service, a database tracking all companies involved in programs covered by the FI library. Richard currently serves as Manager of the Information Services Group (ISG), which develops outbound content for both Forecast International and Military Periscope.