Airbus Reclaims Year-to-Date Delivery Lead // Order Influx Highlights Strong Month for Airbus // 737 MAX Deliveries Outpace Current Target Production Rate

April 2026 Summary

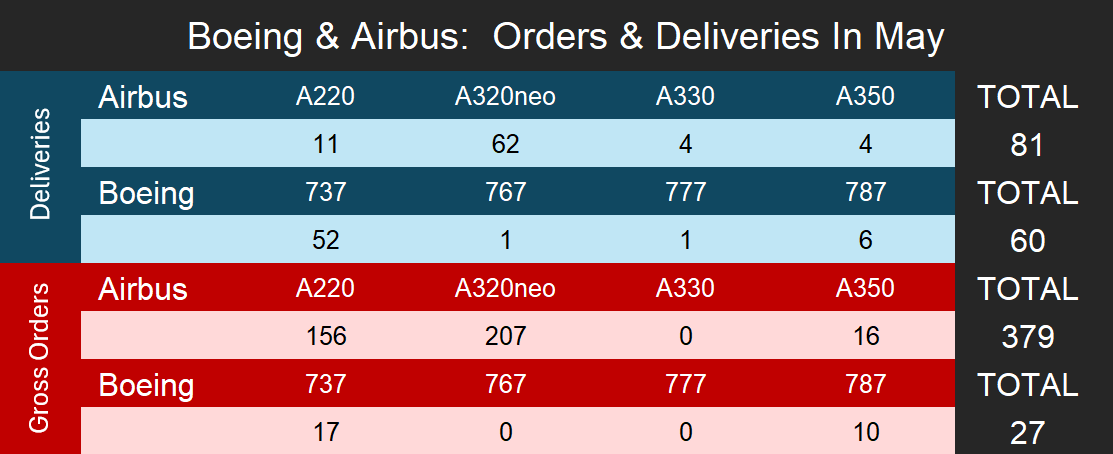

Commercial aircraft delivery and order activity accelerated significantly in May 2026, marked by increased delivery volumes and substantial new fleet commitments for Airbus. Airbus delivered 81 commercial aircraft during the month, up from the 67 units distributed in April, though this increase was supported by a draw from accrued inventory. With this performance, Airbus brought its 2026 cumulative total to 262 deliveries, overtaking Boeing’s year-to-date total of 250. However, this surge did not significantly accelerate the manufacturer’s progress toward hitting its year-end delivery target.

The definitive development of the month was Airbus’s massive order intake, booking 379 gross orders. This volume was driven by 207 orders for the A320neo family and 156 orders for the A220. Meanwhile, Boeing captured only 27 new gross orders during May, which were primarily split between the 737-800A, 737 MAX, and 787-9 programs.

- A320neo numbers include all variants for the family; A319neo, A320neo and A321neo.

Boeing Deliveries

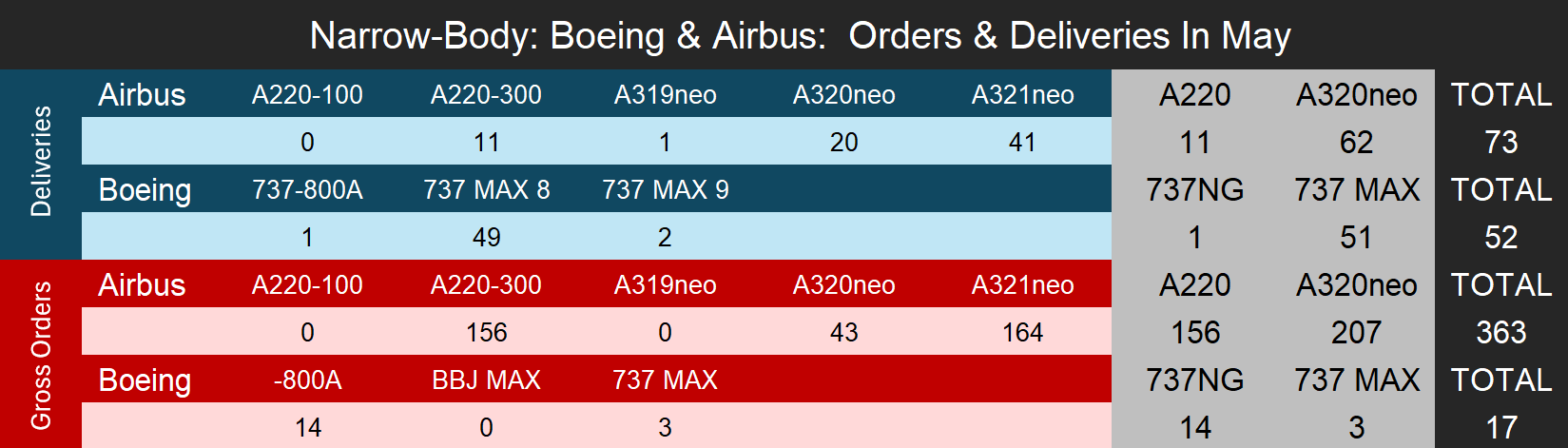

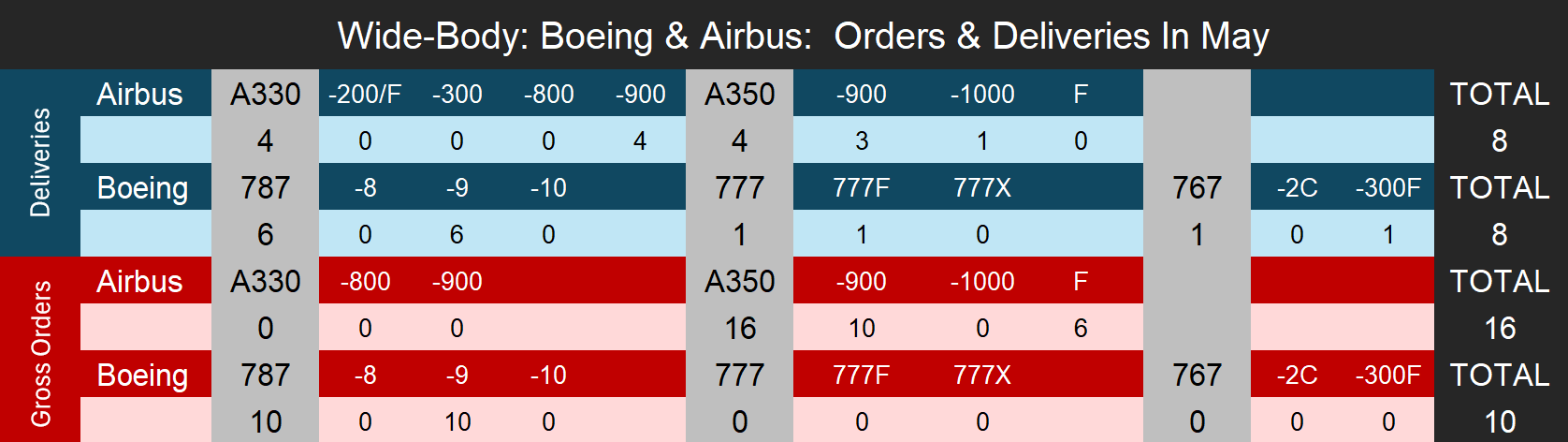

Boeing increased its delivery volume in May, handing over 60 commercial aircraft to customers compared to 47 in the prior month. Single-aisle aircraft accounted for much of this output, with 52 narrowbody jets delivered. This total comprised 49 737 MAX 8s, two 737 MAX 9s, and a single 737-800A. In the widebody segment, Boeing completed eight deliveries: six 787-9 Dreamliners, one 777 Freighter, and one 767-300F.

While this performance raised Boeing’s total 2026 deliveries to 250 aircraft through the end of May, the manufacturer is no longer leading Airbus in total deliveries for the year. After holding the top position through the first four months of the year, Boeing now trails Airbus by 12 aircraft on a year-to-date basis.

Airbus Deliveries

Airbus reported promising results in May, delivering 81 aircraft and logging its highest monthly volume of the year to date. The delivery numbers were anchored by the narrowbody segment, which accounted for 73 single-aisle deliveries, which included 62 A320neo family aircraft (comprising 41 A321neos, 20 A320neos, and one A319neo) and 11 A220-300s. Widebody programs rounded out the monthly total with eight aircraft: four A350s (three -900s and one -1000) and four A330-900s.

Amassing 262 total deliveries through May 31st, Airbus has captured the delivery lead for 2026 in comparison to Boeing. However, while these delivery totals look solid on a surface level, the volume was heavily supported by a drawdown of accrued inventory rather than pure factory output. In terms of actual manufacturing numbers, Airbus only produced around 70% of the aircraft it delivered in May, meaning final deliveries came in significantly higher than actual monthly production. This reliance on stored inventory indicates that while the delivery pace has accelerated, the manufacturer is still working to stabilize baseline production against persistent supply chain disruptions and is likely at risk of missing its delivery target of 870 aircraft for the year.

Boeing Orders

Following strong order activity in April, Boeing’s order intake moderated in May with only 27 gross commitments from customers. New business was led by the narrowbody sector, which secured 17 additional gross orders for the 737 family, of which 14 were for the 737-800A. On the widebody side, the 787-9 added 10 gross orders, while the 767 and 777 programs recorded no new order activity. These transactions bring Boeing’s total 2026 gross order total 324 aircraft through the end of May, which trails Airbus’s total by more than half.

- For consistency, this article does not include Boeing’s ASC 606 accounting adjustments and considers net orders as gross orders minus cancellations.

Airbus Orders

Airbus experienced a substantial shift in commercial demand during May as the manufacturer logged 379 gross orders. This monthly total was heavily weighted toward the single-aisle market, which accounted for 363 narrowbody selections. Activity was driven by a combination of 207 A320neo family orders alongside 156 commitments for the A220. Notably, the A220 program secured its largest single order in years via a landmark agreement with AirAsia for 150 A220-300s, a major transaction that pushes the program past the 1,000 total firm order milestone and increases the backlog to a much healthier level after weak order activity in the previous two years.

The widebody sector provided additional depth to the monthly order total, with Airbus securing 16 gross orders for the A350 program that were split between 10 A350-900 passenger variants and six A350 Freighters. This major influx of new orders lifted the year-to-date gross order tally for Airbus to 815 aircraft through the end of May.

Backlog

As of May 31st, 2026, Airbus reported its total commercial aircraft backlog at 9,247 aircraft, representing a net increase of 276 units from the end of April as the substantial influx of new orders during the month comfortably outpaced deliveries. This extensive order book remains heavily weighted toward the single-aisle market, which now accounts for 7,493 outstanding commitments for the A320neo family alongside 592 orders for the smaller A220 program. The widebody portfolio continues to sustain long-term depth with 1,162 twin-aisle aircraft on order, a total that includes 877 firm commitments for the A350 and 285 for the A330. When evaluated against the manufacturer’s current 2026 delivery target of approximately 870 aircraft, this backlog secures roughly 10.6 years of production coverage for the manufacturer.

In contrast, Boeing’s commercial aircraft backlog contracted slightly to end the month at 6,758 aircraft, marking a minor net decrease of 49 units compared to the figures reported at the close of April. This slight reduction occurred because monthly deliveries surpassed new gross order bookings, though the narrowbody backlog remains strong with 4,819 outstanding narrowbody commitments for the 737 program. On the widebody side of the business, the backlog held steady at a combined 1,939 units, which includes 1,158 orders for the 787 Dreamliner, 692 for the 777 family, and 89 for the 767 platform. Based on current manufacturing paces and our 2026 delivery forecast, Boeing’s overall order book continues to provide the company with approximately 10.1 years of production coverage.

To get a more detailed, month‑by‑month breakdown of commercial aircraft OEM activity, including production, orders, and delivery execution risk, visit https://figlobalintelligence.com/commercial-aircraft-oem-intelligence-brief/

- Airbus backlog numbers do not include A320ceo ghost orders.

- Boeing backlog numbers do not include 737-800 and 777-300ER ghost orders.

- A320neo numbers include all variants for the family; A319neo, A320neo and A321neo

With diverse experience in the commercial aviation industry, Grant joins Forecast International as the Lead Analyst for Commercial Aerospace. He began his career at the Boeing Company, where he worked as a geospatial analyst, designing and building aeronautical navigation charts for Department of Defense flight operations.

Grant then joined a boutique global aviation consulting firm that focused on the aviation finance and leasing industry. In this role he conducted valuations and market analysis of commercial aircraft and engines for banks, private equity firms, lessors and airlines for the purposes of trading, collateralizing and securitizing commercial aviation assets.

Grant has a deep passion for the aviation industry and is also a pilot. He holds his Commercial Pilots License and Instrument Rating in addition to being a FAA Certified Flight Instructor.