Airbus Widens Mid-Year Delivery Lead over Boeing // 737 MAX Deliveries Reach Current Production Target // Strong Order Rebound Refuels Boeing’s Commercial Sales

SAS A330neo. Image – Airbus

June 2026 Summary

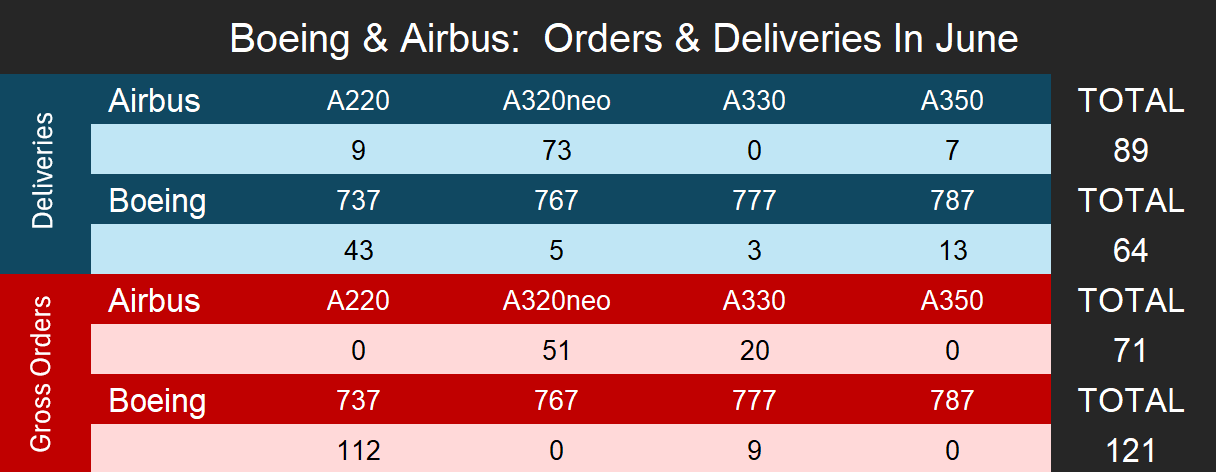

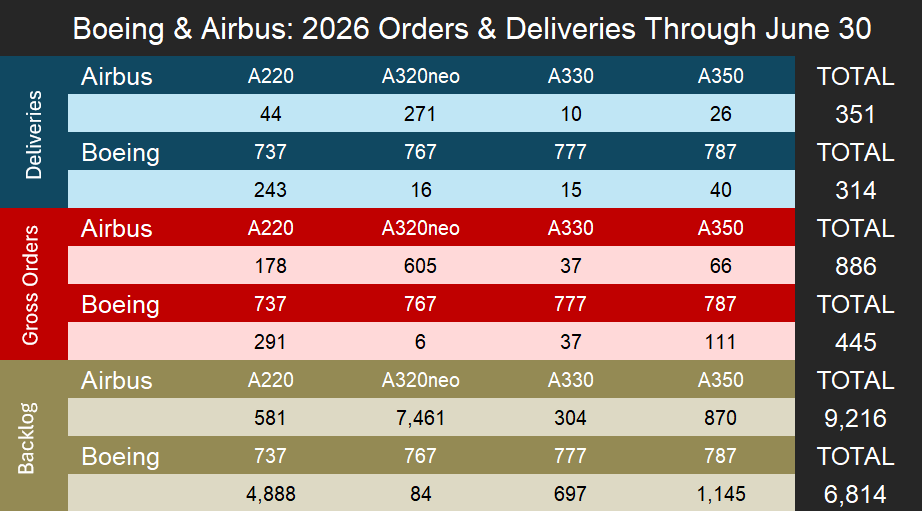

Commercial aircraft delivery and order activity further strengthened in June 2026. Airbus delivered 89 commercial aircraft during the month, representing a step up from the 81 units handed over in May. With this performance, Airbus pushed its cumulative 2026 deliveries to 351, extending its lead over Boeing, which reached a year-to-date total of 314 aircraft. This strong monthly showing leaves Airbus only slightly behind the pace required to meet its annual delivery goal. It marks a notable recovery after a disappointing start to the year, when Airbus lagged so far behind its delivery targets that a downward revision to its annual objective seemed increasingly likely.

While Airbus maintained its delivery dominance, Boeing led the monthly sales in June. Boeing secured 121 new gross orders in June, driven primarily by strong commitment in its 737 MAX line. In contrast, Airbus experienced a quieter month for sales, recording 71 gross orders, which is a noticeable deceleration from its massive May bookings. Of these 71 gross orders, 51 of them were for the A320neo family of aircraft.

Notes:

- A320neo numbers include all variants for the family; A319neo, A320neo and A321neo.

Boeing Deliveries

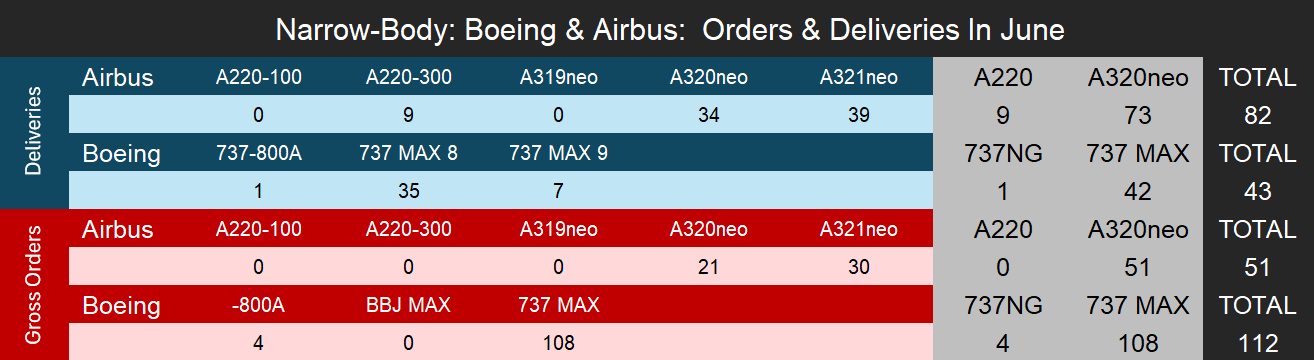

Boeing stepped up its monthly delivery rate in June, handing over 64 commercial jets compared to 60 in May. The single-aisle sector remained the primary driver with 43 narrowbody 737s delivered, a total that included 35 737 MAX 8s, seven 737 MAX 9s, and a single 737-800A. While the FAA-approved rate of 42 aircraft per month is a production cap rather than a delivery target, Boeing reaching 42 MAX deliveries in June is a highly encouraging sign. This suggests that final assembly output is trending toward stabilization at this rate, especially as Boeing transitions away from relying on stored MAX inventory to support deliveries of the aircraft. Deliveries of the MAX are now becoming much better aligned with newly produced aircraft rolling off the final assembly line.

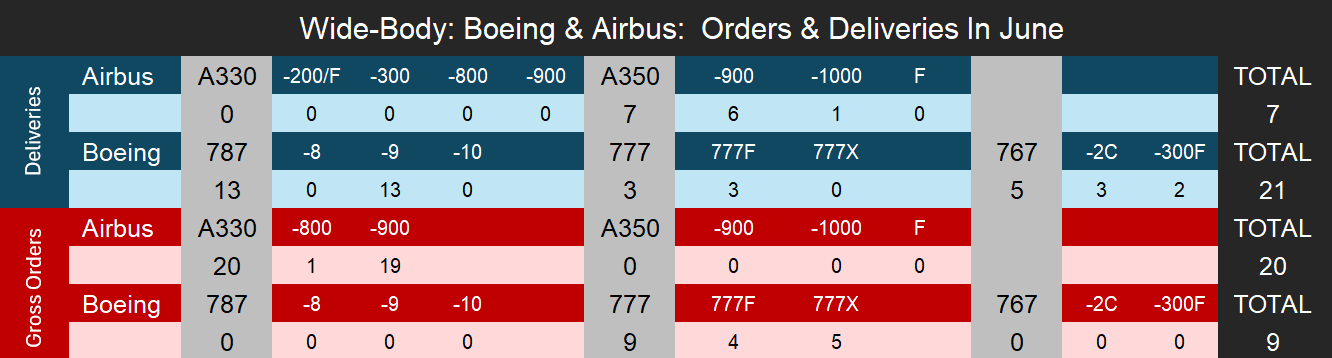

On the widebody side, Boeing recorded a notable increase by delivering 21 twin-aisle aircraft. This segment consisted of 13 787-9 Dreamliners, five 767s (comprising three -2C variants and two -300Fs), and three 777 Freighters. The 13 Dreamliner were expected and align with our previous projections, as the program continues to draw down its substantial backlog of built inventory despite current production rates remaining below the current target rate. Because 787 inventory remains elevated, the trend of delivery volumes outpacing production is expected to persist for the near future. Additionally, while the June results raised Boeing’s 2026 year to date deliveries to 314, the US manufacturer continues to trail its European rival. After losing its lead at the end of May, Boeing now lags Airbus by 37 aircraft on a year to date basis.

Airbus Deliveries

Airbus registered another strong month, delivering 89 jets in June to achieve its highest monthly output of 2026 so far. The narrowbody lineup drove the bulk of this activity with 82 single-aisle deliveries. This segment included 73 A320neo family aircraft (comprising 39 A321neos and 34 A320neos) along with nine A220-300s. The widebody segment added seven aircraft to the monthly total, all belonging to the A350 family, specifically six A350-900s and one A350-1000.

By accumulating 351 total deliveries in the first half of the year, Airbus cemented its delivery lead for 2026 over Boeing and put itself back on track to reach its annual target of 870 deliveries. Additionally, the manufacturer is internally targeting 900 deliveries for the year. While achieving this goal remains possible, we are skeptical because Airbus production has been volatile over the past two years. Many programs are not yet operating at a stable rate and rely heavily on drawing down stored inventory. These ongoing swings in assembly and delivery rates make it difficult to reliably gauge progress toward the company’s ultimate goals.

Boeing Orders

Following a quiet May, orders for Boeing aircraft rebounded sharply in June with 121 new gross commitments. The narrowbody segment captured most of this demand, logging 112 commitments for the 737 family. This consisted of 108 737 MAX jets and four 737-800As.

On the widebody side, Boeing booked nine gross orders for the 777 program. These were split between five 777X models and four 777 Freighters, while the 767 and 787 programs saw no new order activity. This pushed Boeing’s year to date gross orders to 445 aircraft through June 30th, closing some of the gap with Airbus. However, the US manufacturer still lags Airbus by 441 gross orders, as its European competitor holds nearly double Boeing’s total for the year.

- For consistency, this article does not include Boeing’s ASC 606 accounting adjustments and considers net orders as gross orders minus cancellations.

Airbus Orders

After strong performance in May, Airbus’s order intake moderated to 71 gross commitments in June. This monthly sales volume was led by the single-aisle market, which booked 51 narrowbody orders, all for the A320neo family, and consisted of 30 A321neos and 21 A320neos.

The widebody segment contributed 20 gross orders, highlighted by 19 A330-900s and one A330-800, while the A350 and A220 programs logged no new orders during this period. These additions brought Airbus’s cumulative 2026 gross order book to 886 aircraft at the mid-year mark. This total comfortably outpaces Boeing’s sales performance and has expanded Airbus’s backlog by approximately 535 aircraft this year, excluding any order cancellations.

Backlog

- Airbus backlog numbers do not include A320ceo ghost orders.

- Boeing backlog numbers do not include 777-300ER ghost orders.

- A320neo numbers include all variants for the family; A319neo, A320neo and A321neo

By the close of the first half of 2026, the active order book at Airbus stood at 9,216 commercial aircraft. This mid-year figure represents a minor reduction of 31 units compared to the previous month, as a highly productive delivery period slightly outpaced new orders in both May and June. Narrowbodies continue to dominate the manufacturer’s total backlog, with the A320neo family accounting for 7,461 outstanding orders alongside 581 commitments for the smaller A220 program. On the widebody side of the business, Airbus holds 1,174 twin-aisle aircraft on order, a total comprising 870 firm commitments for the A350 and 304 for the A330. Airbus’ backlog now translates to roughly 10.6 years of production coverage when measured against the company’s current annual delivery target of 870 aircraft.

Meanwhile, Boeing saw its total commercial backlog expand to 6,814 aircraft at the end of June. The net increase of 56 units over May’s closing numbers was driven by a strong month of new sales that ended up outpacing deliveries. The foundation of Boeing’s order book remains the narrowbody segment, which is anchored by 4,888 outstanding commitments for the 737 program. Boeing’s widebody portfolio accounts for 1,926 units of the remaining aircraft, led by 1,145 orders for the 787 Dreamliner, 697 for the 777 family, and 84 for the 767 platform. Under current production rates and our projected 2026 delivery total for Boeing, the manufacturer’s current backlog provides approximately 10.2 years of production coverage.

To get a more detailed, month‑by‑month breakdown of commercial aircraft OEM activity, including production, orders, and delivery execution risk, visit https://figlobalintelligence.com/commercial-aircraft-oem-intelligence-brief/

With diverse experience in the commercial aviation industry, Grant joins Forecast International as the Lead Analyst for Commercial Aerospace. He began his career at the Boeing Company, where he worked as a geospatial analyst, designing and building aeronautical navigation charts for Department of Defense flight operations.

Grant then joined a boutique global aviation consulting firm that focused on the aviation finance and leasing industry. In this role he conducted valuations and market analysis of commercial aircraft and engines for banks, private equity firms, lessors and airlines for the purposes of trading, collateralizing and securitizing commercial aviation assets.

Grant has a deep passion for the aviation industry and is also a pilot. He holds his Commercial Pilots License and Instrument Rating in addition to being a FAA Certified Flight Instructor.