Inventory Clearance Drives Delivery Increase /// Widebody Lead Times Improve /// Narrowbody Production Continues to Lag

737 MAX Renton Factory – Boeing

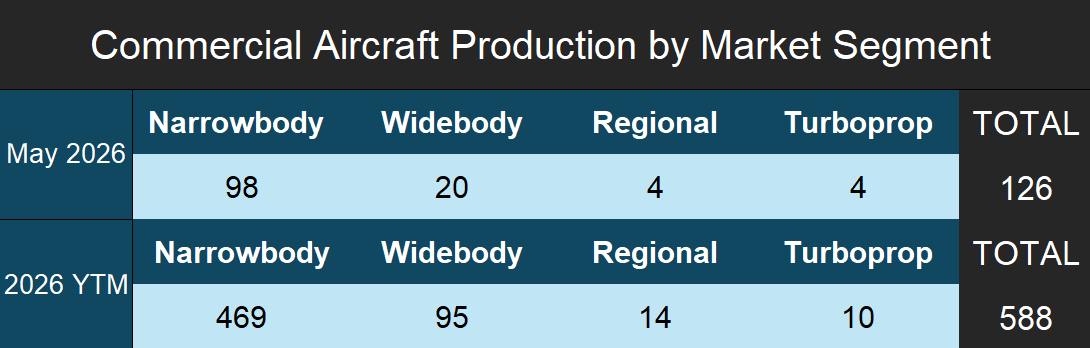

Production by Market Segment

Commercial aircraft manufacturing levels experienced a decrease in May 2026, dropping to 126 units from the 133 assembled during April and interrupting the upward trajectory established earlier in the spring. Dominating the month’s manufacturing activity, narrowbody assembly lines turned out 98 aircraft, representing a five-unit decrease from April’s total of 103. The widebody category also contributed to the overall monthly decline, slipping from 24 units down to 20. This pullback follows an acceleration across several major programs during the prior month, which subsequently failed to reach those same levels in May. In the regional aviation sectors, manufacturers completed four regional jets, while the turboprop segment matched that volume with four units. Looking at the broader picture, year-to-month (YTM) production now stands at 588 aircraft for the first five months of the year. Single-aisle aircraft remain the primary market driver with 469 aircraft produced, followed by 95 widebodies. Regional aircraft and turboprops continue to serve as minor contributors to the annual total, tracking at 14 and 10 units, respectively.

- Production data represents the actual number of aircraft produced in May 2026. Forecast International considers an aircraft produced upon its first flight. This may differ from an OEM’s definition of produced.

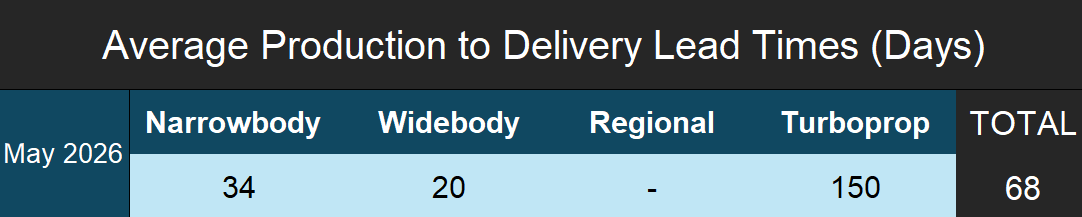

Average Production-to-Delivery Lead Times

The timeline spanning production to final delivery experienced varied shifts during May. Single-aisle aircraft continue to face operational headwinds as average lead times expanded to 34 days, representing a three-day extension beyond April’s 31-day average, and up from an average of 24 days in March. Ongoing production bottlenecks plaguing the A320neo program are primarily responsible for this slowdown, creating inventory backlogs and complicating efforts to maintain an accelerated delivery pace, even as the 737 MAX achieves higher output.

On the other hand, widebody lead times improved to a 20-day average, falling just under the 23 days logged the previous month. However, this data point does not tell the whole story regarding widebody manufacturing health. While lead times have compressed, this drop is occurring alongside falling production rates. Boeing and Airbus are managing to push out this lower volume of units highly efficiently from assembly to delivery, yet most programs are still failing to meet their current target production rates. Nevertheless, the improved lead time serves as a positive leading indicator, signaling that the manufacturers have established the baseline operational efficiency necessary to recover and hit their current production targets.

Meanwhile, turboprop lead times reached 150 days, a level indicative of the long-cycle delivery schedules typical for that segment. Regional jet data went unrecorded due to a lack of paired delivery events. Averaged across all segments, the industry recorded a 68-day lead time for the month, which was heavily influenced by the Turboprop lead times. Across Narrowbody and Widebody aircraft, the average lead time was 27 days in the month of May.

Projected Deliveries

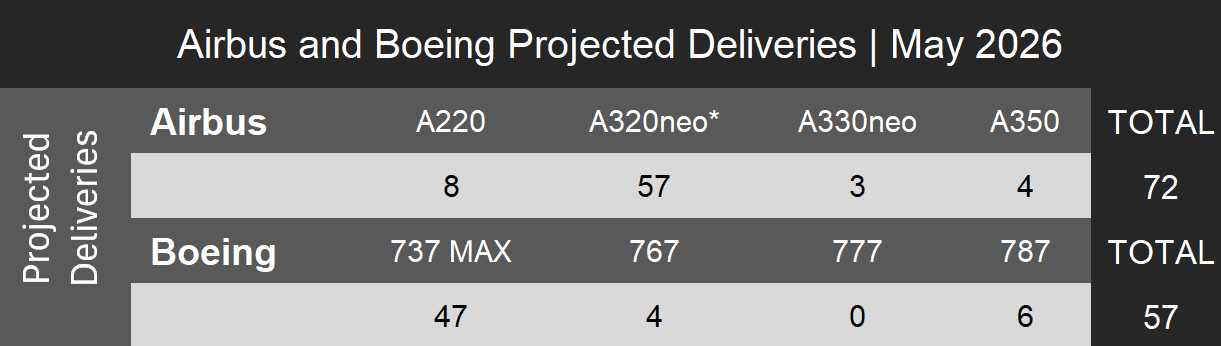

May delivery estimates from Forecast International indicate that Airbus and Boeing delivered approximately 129 aircraft during the month, climbing past the 114 units both manufacturers delivered in April.

Of this total, Airbus handed over 72 airframes. The A220 line enjoyed a strong month with eight deliveries, effectively doubling its April performance, while the A320neo family maintained upward momentum by delivering a total of 57 aircraft. Most importantly, the increase in narrowbody deliveries was mainly driven by clearing already produced inventory rather than an increase in the production rate of the A320neo family. On the widebody side, Airbus’ results remained light with three A330neos and four A350s delivered, as the A350 program in particular continues to struggle and shows no signs of near-term improvement.

As for Boeing, the manufacturer registered an estimated 57 deliveries, showing strong growth over the 47 aircraft recorded in April. Driving this increase was 47 737 MAX models, driven by a production ramp-up near its current target rate of 42 aircraft per month. Meanwhile, Boeing’s widebody programs maintained steady delivery rates, handing over six 787s, four 767s, and zero 777s.

Notes:

- Delivery data is the expected number that Boeing and Airbus will report in their May 2026 Orders and Deliveries summary and is based on Forecast International’s internal research. Numbers are not official and are not provided by Airbus or Boeing.

- A320neo numbers include all variants for the family; A319neo, A320neo and A321neo

To get a more detailed, month‑by‑month breakdown of commercial aircraft OEM activity, including production, orders, and delivery execution risk, visit https://figlobalintelligence.com/commercial-aircraft-oem-intelligence-brief/

With diverse experience in the commercial aviation industry, Grant joins Forecast International as the Lead Analyst for Commercial Aerospace. He began his career at the Boeing Company, where he worked as a geospatial analyst, designing and building aeronautical navigation charts for Department of Defense flight operations.

Grant then joined a boutique global aviation consulting firm that focused on the aviation finance and leasing industry. In this role he conducted valuations and market analysis of commercial aircraft and engines for banks, private equity firms, lessors and airlines for the purposes of trading, collateralizing and securitizing commercial aviation assets.

Grant has a deep passion for the aviation industry and is also a pilot. He holds his Commercial Pilots License and Instrument Rating in addition to being a FAA Certified Flight Instructor.