Boeing Continues to Lead Airbus in Year-to-Date Deliveries // Order Surge Bolsters Boeing Backlog // Airbus Maintains Slim Narrowbody Delivery Lead

April 2026 Summary

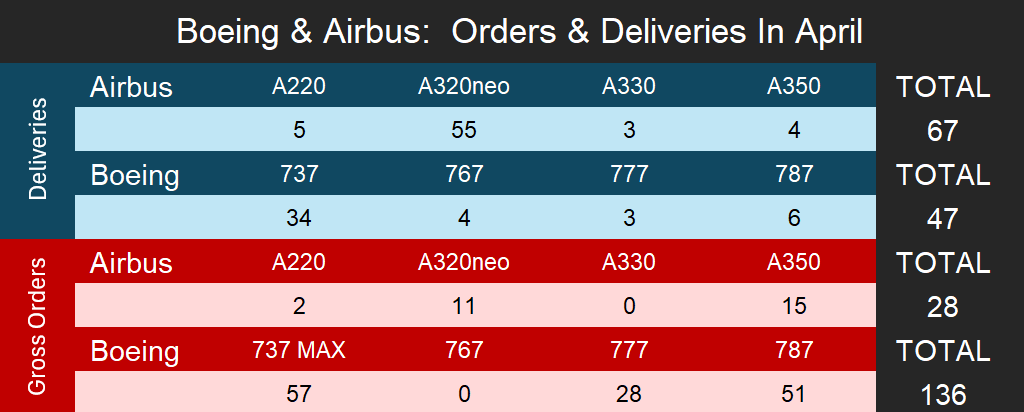

The landscape in April 2026 was defined by a significant contrast between delivery volumes and new order activity. Airbus maintained its position as the monthly delivery leader, transferring 67 aircraft to customers, which represents a step up from its March performance of 60 deliveries. However, Boeing remains the year-to-date leader for 2026 with 190 total deliveries compared to only 181 for Airbus. This puts Boeing well on track to meet our yearly delivery forecast, while Airbus continues to remain behind pace to hit its annual target. The primary headline for the month was Boeing’s strong order intake, which was led by 57 orders for the 737 MAX. The manufacturer secured 136 gross orders, nearly doubling its total for the entire first quarter. On the other hand, Airbus recorded a lighter month with 28 new gross orders.

Notes:

- A320neo numbers include all variants for the family; A319neo, A320neo and A321neo.

Boeing Deliveries

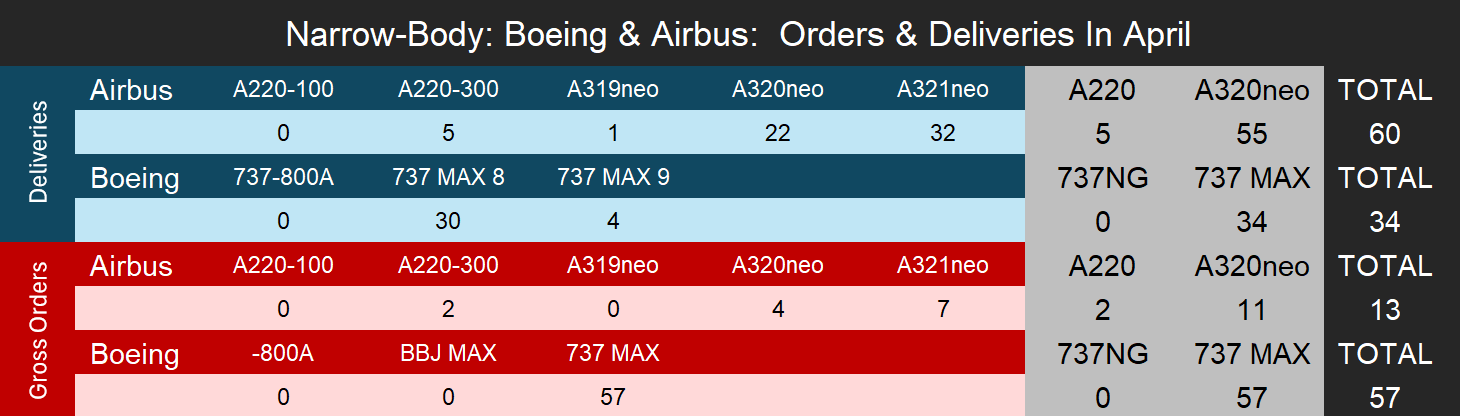

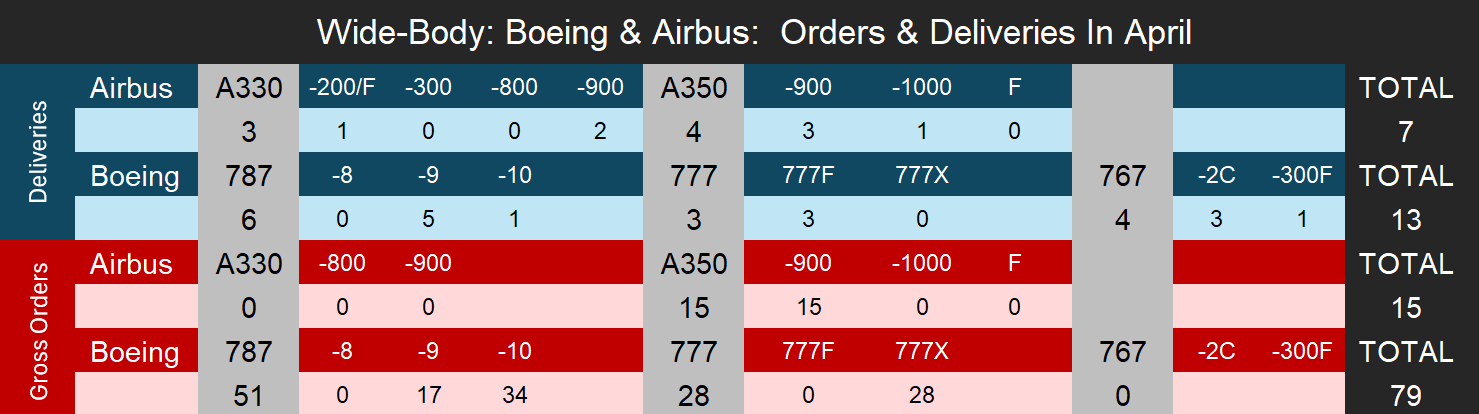

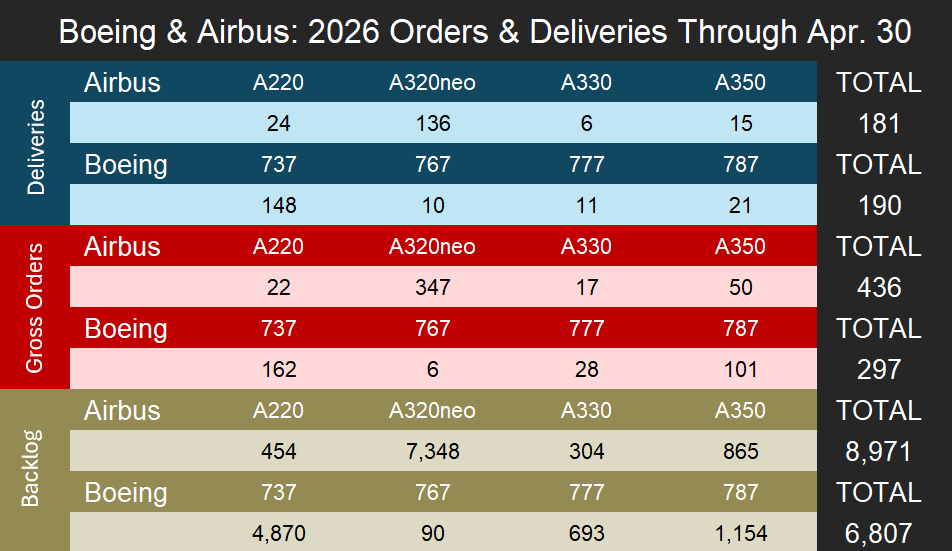

Boeing’s delivery performance in April remained resilient with 47 total aircraft handed over to customers. The narrowbody segment accounted for 34 units, all of which were from the 737 MAX family, specifically featuring 30 MAX 8 and four MAX 9 variants. On the widebody side, Boeing recorded 13 deliveries, a total supported by six 787 Dreamliners, three 777 Freighters, and four 767s. The 767 volume was notably split between three -2C variants and a single -300F, reflecting the continued demand for the multi-role platform as dedicated cargo deliveries come to an end. This consistent monthly output brings Boeing’s year-to-date delivery total to 190 aircraft, allowing the manufacturer to maintain its position as the industry delivery leader through the first four months of 2026. By ending the month nine units ahead of Airbus in cumulative deliveries, Boeing has demonstrated a strong operational pace that puts it on path to meet our delivery forecast for the year.

Airbus Deliveries

Airbus demonstrated an upward trend in its delivery performance for April, handing over 67 commercial aircraft to customers and marking its strongest monthly result of the year thus far. This increase was driven primarily by a narrowbody recovery, with 60 single-aisle jets delivered, including 55 aircraft from the A320neo family and five A220-300s. The widebody segment contributed an additional seven units to the monthly total, consisting of four A350s, split between three -900s and one -1000, alongside three A330 aircraft. While these 67 deliveries indicate that Airbus is gaining momentum as it moves into the second quarter, the year-to-date total of 181 aircraft still highlights the ongoing challenge of closing the gap with Boeing’s lead. The manufacturer remains focused on stabilizing its production lines to overcome persistent supply chain constraints, particularly as it continues to push toward its “Rate 75” target for the A320neo program.

Boeing Orders

Boeing recorded strong order activity during April, booking 136 gross orders and marking a significant increase from the 33 units reported in March. This month’s intake was heavily weighted toward the manufacturer’s widebody portfolio, highlighted by 51 new orders for the 787 Dreamliner and 28 orders for the 777X family. The narrowbody segment also saw healthy demand with 57 new commitments for the 737 MAX program, further growing the backlog for the program. This influx of orders brings Boeing’s year-to-date gross order total to 297 aircraft through the end of April.

- For consistency, this article does not include Boeing’s ASC 606 accounting adjustments and considers net orders as gross orders minus cancellations.

Airbus Orders

Following a surge in March, order intake slowed significantly in April with 28 new gross orders. The month’s activity was led by the widebody segment, which saw 15 new orders for the A350-900. In the narrowbody sector, Airbus added 11 orders for the A320neo family and two additional units for the A220-300 to its books. These latest agreements bring the company’s year-to-date gross order total to 436 aircraft by the end of April.

Backlog

- Airbus backlog numbers do not include A320ceo ghost orders.

- Boeing backlog numbers do not include 737-800 and 777-300ER ghost orders.

- A320neo numbers include all variants for the family; A319neo, A320neo and A321neo

As of April 30th, 2026, Airbus reported a commercial aircraft backlog of 8,971 aircraft, representing a decrease of 60 units from the end of March. The backlog remains heavily concentrated in the narrowbody segment with 7,348 A320neo family aircraft, while the widebody book continues to show strength with 1,169 aircraft on order across the A350 and A330 programs. At the current 2026 delivery target of 870 aircraft, this total backlog provides Airbus with approximately 10.3 years of production coverage.

In contrast, Boeing’s commercial backlog grew to 6,807 aircraft by the end of April 30th, an increase of 88 units compared to the figures reported at the end of March. This growth was driven by a substantial surge in new order activity, where the 136 gross orders booked exceeded the 47 aircraft delivered during the month. The 737 MAX remains the primary driver of Boeing’s order book with 4,870 outstanding orders, while the widebody segment strengthened to 1,937 units following new orders for the 787 and 777X. Based on current production estimates, Boeing’s backlog now equates to roughly 10.2 years of production coverage.

To get a more detailed, month‑by‑month breakdown of commercial aircraft OEM activity, including production, orders, and delivery execution risk, visit https://figlobalintelligence.com/commercial-aircraft-oem-intelligence-brief/

With diverse experience in the commercial aviation industry, Grant joins Forecast International as the Lead Analyst for Commercial Aerospace. He began his career at the Boeing Company, where he worked as a geospatial analyst, designing and building aeronautical navigation charts for Department of Defense flight operations.

Grant then joined a boutique global aviation consulting firm that focused on the aviation finance and leasing industry. In this role he conducted valuations and market analysis of commercial aircraft and engines for banks, private equity firms, lessors and airlines for the purposes of trading, collateralizing and securitizing commercial aviation assets.

Grant has a deep passion for the aviation industry and is also a pilot. He holds his Commercial Pilots License and Instrument Rating in addition to being a FAA Certified Flight Instructor.