Inventory Drawdown Drives Delivery Increase /// Widebody Lead Times Deteriorate /// Narrowbody Production Recovers and Surpasses Targets

737 MAX Renton Factory. Image – Boeing

For the purposes of this article, Forecast International considers an aircraft to be “produced” once it completes its first test flight, and “delivered” when it is contractually handed over to the customer.

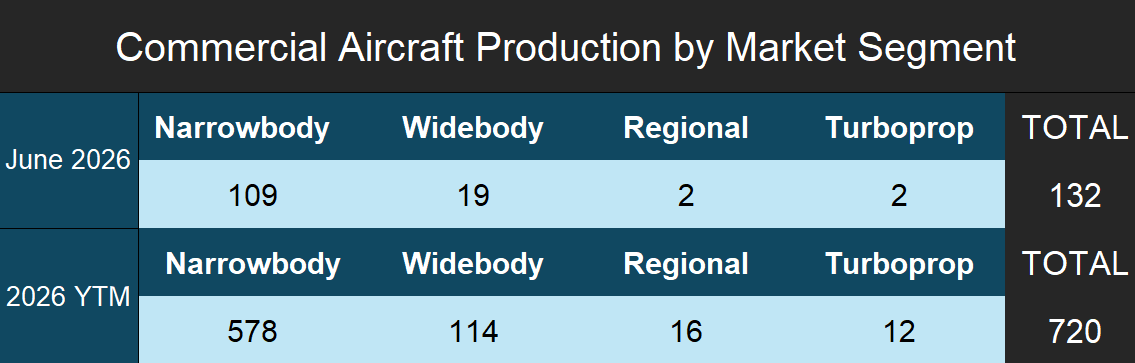

Production by Market Segment

Commercial aircraft manufacturing experienced a slight increase in June 2026, climbing to 132 units after 126 aircraft produced in May and 133 in April. As expected, single-aisle manufacturing made a recovery, with OEMs producing 109 narrowbody aircraft, an 11-unit increase over May’s output of 98. This was mainly due to A320neo manufacturing, which finally surpassed its current target rate of 50 aircraft per month after struggling to meet its target rate in previous months of the year. Meanwhile, widebody production remained entirely flat, matching the 19 units produced during the previous month. Within the smaller sectors, regional jet manufacturers produced two aircraft, which is identical to the two units completed by the turboprop segment. Looking at the broader mid-year picture, total year-to-month (YTM) production has reached 720 aircraft over the first half of the year. Narrowbodies continue to drive this volume with 578 units built, compared to 114 widebody aircraft completions, while regional aircraft and turboprops are tracking at 16 and 12 units, respectively.

- Production data represents the actual number of aircraft produced in June 2026. Forecast International considers an aircraft produced upon its first flight. This may differ from an OEM’s definition of produced.

Average Production-to-Delivery Lead Times

During June, the timeline spanning production to final delivery varied across all market segments. For single-aisle aircraft, operational headwinds began to ease as average lead times dropped to 27 days, which marked a seven-day improvement from the 34-day average seen in May and sat below the 31-day average from April. The long-standing production bottlenecks that previously plagued the A320neo program showed signs of clearing, which helped reduce inventory backlogs and supported a quicker delivery pace while the 737 MAX also continues to show healthy levels of production.

On the other hand, widebody lead times grew much longer, stretching to a 68-day average and rising sharply above the 20 days logged the previous month. This was driven by both the A350 and 787 programs, which saw a clearing of inventory that contributed to these higher lead times, with a substantial number of aircraft delivered in June between 60 to 90 days after their initial first test flight. This increase in lead times also happened alongside flat production rates as Airbus and Boeing continue to deliver accumulated inventory on these programs, and most widebody programs are still failing to meet their current target production rates. Even so, the expanded lead time serves as a critical indicator for Airbus and Boeing’s widebody programs because it signals that they are continuing to experience operational bottlenecks that are preventing their widebody programs from consistently reaching their current production targets and are instead relying on accumulated inventory to support delivery numbers.

Projected Deliveries

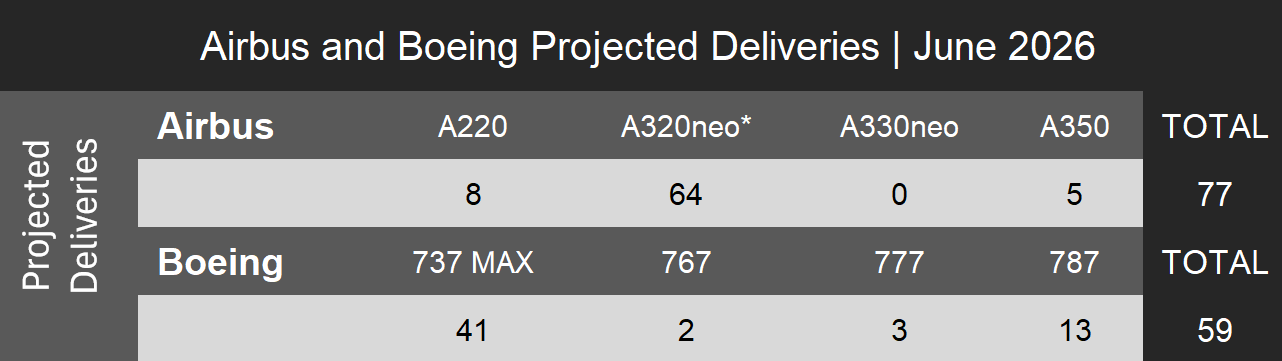

According to June delivery tracking from Forecast International, Airbus and Boeing delivered an estimated 136 aircraft combined during the month, slightly increasing from the 129 units distributed by both manufacturers throughout May.

Airbus accounted for 77 airframes out of this overall monthly figure, with the A220 line maintaining a steady rate by matching its May performance with eight deliveries, while the A320neo family built additional momentum as a total of 64 aircraft were handed over to customers. Most importantly, a mix between clearing already produced inventory and a slight acceleration in the production rate of the A320neo family was what mainly drove this increase in narrowbody deliveries. On the widebody side, results remained light for Airbus with zero A330neos and five A350s delivered, as near-term improvement shows no signs of appearing for the struggling A350 program. Though Airbus hasn’t released its official June results yet, broader industry expectations point toward around 89-90 deliveries, meaning our estimate came in lower because of our specific methodology in terms of how we calculate deliveries. Regardless of these calculation differences, deliveries remained strong for Airbus in June, which serves as a good sign that pushes the manufacturer closer to being on path with its annual target, even though accumulated inventory and its subsequent drawdown partially drove June’s delivery numbers.

Shifting focus over to Boeing, the manufacturer continued to deliver at a consistent pace, with our estimates indicating that they delivered approximately 59 aircraft in June compared to 57 aircraft in May. Driving this single-aisle volume was 41 737 MAX models, a pace that successfully kept Boeing’s overall delivery rate aligned near its current target rate of 42 aircraft per month. Delivery rates mainly varied across Boeing’s widebody programs, which saw 13 787s, two 767s, and three 777s delivered to operators, with the 787 deliveries increasing above the program’s current production target rate because of a drawdown in inventory rather than any meausred increase in production.

Notes:

- Delivery data is the expected number that Boeing and Airbus will report in their June 2026 Orders and Deliveries summary and is based on Forecast International’s internal research. Numbers are not official and are not provided by Airbus or Boeing.

- A320neo numbers include all variants for the family; A319neo, A320neo and A321neo

To get a more detailed, month‑by‑month breakdown of commercial aircraft OEM activity, including production, orders, and delivery execution risk, visit https://figlobalintelligence.com/commercial-aircraft-oem-intelligence-brief/

With diverse experience in the commercial aviation industry, Grant joins Forecast International as the Lead Analyst for Commercial Aerospace. He began his career at the Boeing Company, where he worked as a geospatial analyst, designing and building aeronautical navigation charts for Department of Defense flight operations.

Grant then joined a boutique global aviation consulting firm that focused on the aviation finance and leasing industry. In this role he conducted valuations and market analysis of commercial aircraft and engines for banks, private equity firms, lessors and airlines for the purposes of trading, collateralizing and securitizing commercial aviation assets.

Grant has a deep passion for the aviation industry and is also a pilot. He holds his Commercial Pilots License and Instrument Rating in addition to being a FAA Certified Flight Instructor.