Solid Month for Plane Makers Despite Large Airbus A330 Cancellation.

Airbus and Boeing Report Significant Dependence on Russian Titanium.

by J. Kasper Oestergaard, European Correspondent, Forecast International.

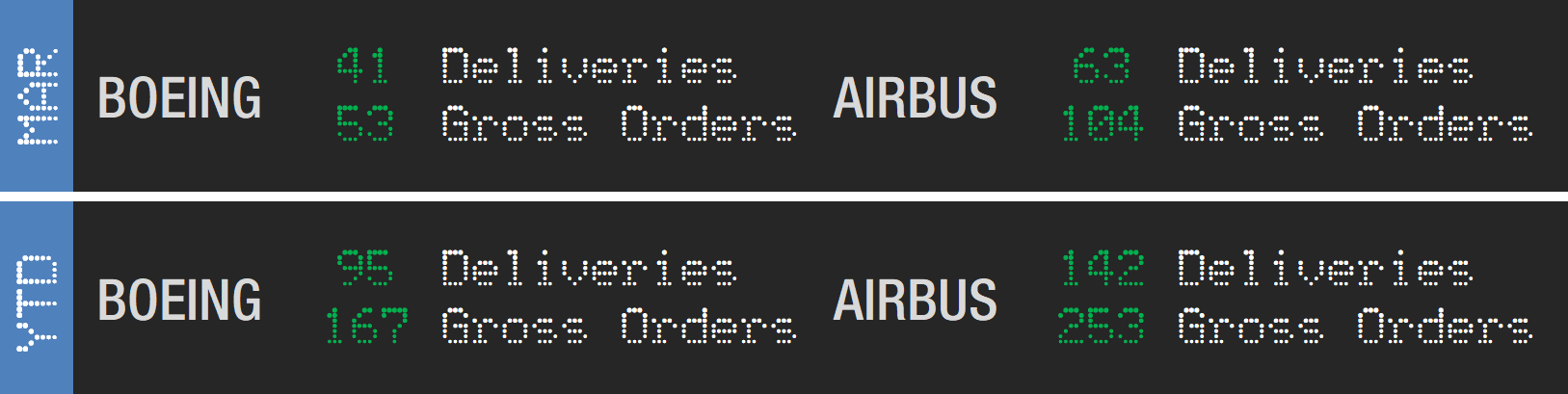

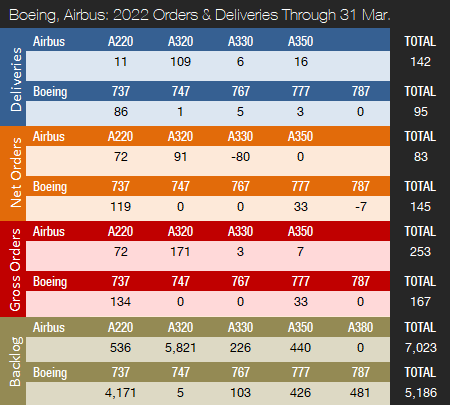

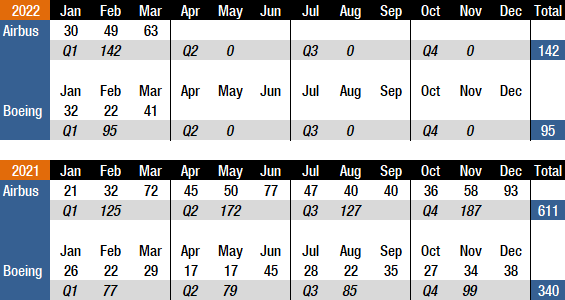

Boeing and Airbus delivered 41 and 63 commercial jets in March 2022, compared to 29 and 72 deliveries, respectively, in the same month last year. Year-to-date, Boeing and Airbus have delivered 95 and 142 aircraft, compared to 77 and 125, respectively, in the first quarter of 2021. After the first three months of the year, Boeing and Airbus were 18 and 17 deliveries, respectively, ahead of last year’s totals to date.

Following a more than challenging 2020 due to the COVID-19 pandemic, 2021 was a year of recovery for the two largest commercial plane makers. 2022 is well underway and is expected to be another year of recovery for the commercial aircraft manufacturing industry, despite events currently unfolding in Ukraine. Boeing and Airbus still have a long way to go before deliveries are back to pre-pandemic levels, though. For the full year 2021, Boeing delivered 340 aircraft, compared to 157 and 380 in 2020 and 2019, respectively. Boeing’s last “normal” year was 2018 – before COVID and the 737 MAX grounding – when it delivered 806 jets, a level that will likely not be recaptured before 2024 or 2025. The past three years have been extremely challenging for Boeing but, despite ongoing Dreamliner quality issues, the outlook is now looking brighter than at any time since March 2019, when the second 737 MAX crash occurred. Orders are strong and deliveries have surged from the 2020 lows, with another sharp increase expected this year. The 737 MAX, however, remains grounded in China nearly 18 months after the U.S. Federal Aviation Administration (FAA) ungrounded the aircraft in November 2020. While not involving a 737 MAX, the March 21 crash of China Eastern Airlines Flight 5735, a Boeing 737-800, certainly has not helped in Boeing’s efforts to restore confidence in the 737 MAX in China. The crash could potentially delay the return of the aircraft, according to some sources.

In 2021, Airbus delivered 611 aircraft and won the deliveries crown for the third year in a row. Deliveries were up from 566 in 2020 but remain well below the company’s all-time record high of 863 shipments in 2019. Airbus is expected to retain the deliveries lead for the foreseeable future due to the company’s comfortable backlog lead over its American rival. Prior to 2019, Boeing had out-delivered Airbus every year since 2012.

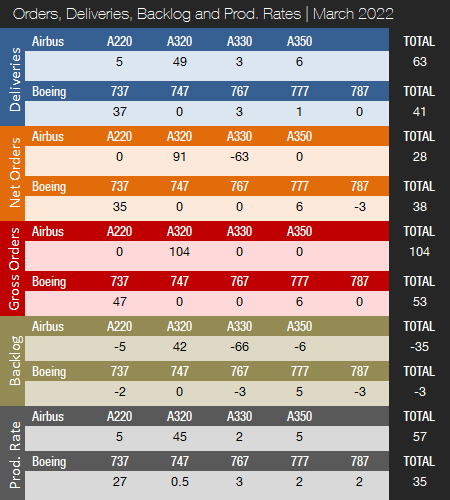

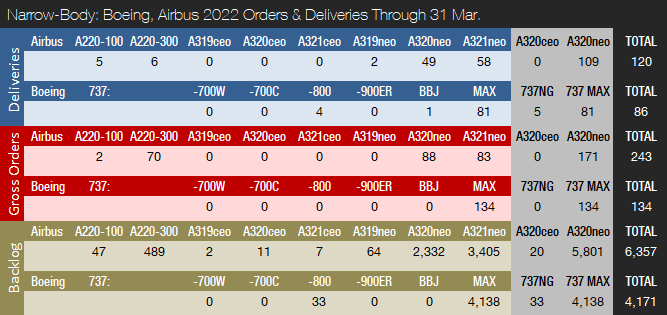

As indicated above, in March 2022, Boeing delivered 41 jets, including 37 737s (35 MAX / 2 NG), three 767s, and one 777F. The 737 program is currently officially producing at a rate of 27 per month, up from 19 as of the end of October 2021, and is close to reaching a near-term target of 31 per month. According to Reuters, Boeing has preliminary plans to boost 737 production to 38 jets per month in the first half of 2023, followed by another increase to 47 jets per month by the end of 2023.

Dreamliner deliveries have now been suspended for nearly a year, and it is unknown when shipments will resume. Boeing suspended Dreamliner deliveries in May 2021 for the second time in less than a year. The FAA is reviewing Boeing’s method for inspecting and evaluating the aircraft to ensure it meets federal safety regulations. In February, the head of the FAA, Steve Dickson, stated that the agency needs a “systemic fix” from Boeing to address Dreamliner production issues and would not allow the company to self-certify individual new jets when deliveries resume. However, the FAA has acknowledged that Boeing is heading in the right direction. The FAA wants Boeing to ensure it has a robust plan for the rework that it performs on a large number of new 787s in storage and demonstrate that its delivery processes are stable. According to Boeing, the company is continuing to complete comprehensive inspections across the 787 production system and within the supply chain, while holding detailed, transparent discussions with the FAA, suppliers, and customers. The company continues to perform rework on 787 airplanes in inventory and is engaged in detailed discussions with the FAA. At the end of last year, Boeing had 110 Dreamliners in storage (manufactured but not yet certified). The current 787 production rate is approximately two aircraft per month, and Boeing expects to continue at this rate until deliveries resume and then return to five per month over time. In March, it was reported that the company is currently testing the ability of suppliers to meet output scenarios as high as seven per month by the end of 2023.

The 777 program will get a new addition in late 2023 with the first delivery of the 777X, and Boeing announced recently that it will increase the 777/777X production rate from two to three per month in 2022. In January this year, Boeing launched a new 777X-based freighter, thereby expanding its 777X and cargo portfolio. Qatar Airways will be the 777-8F launch customer.

In March 2022, Airbus delivered 63 jets, including five A220s, 49 A320s (all NEO), three A330s, and six A350s. During 2021, Airbus steadily increased A320 production from 40 per month to 43 in Q3 2021 before finishing the year at a rate of 45 per month. Production will continue to be increased until reaching a monthly rate of 65 by the summer 2023. Airbus has also discussed a scenario with a rate of 70 by Q1 2024. Longer-term, the company is investigating opportunities for rates as high as 75 by 2025. The A220, meanwhile, is being produced at a rate of five aircraft per month. The rate will be increased to six in the coming months – with a monthly production rate of 14 envisioned by the middle of the decade. The A350 production rate currently averages five per month and will be increased to six by early 2023. Airbus is currently producing two A330s per month, a rate that will be increased to nearly three aircraft by the end of 2022.

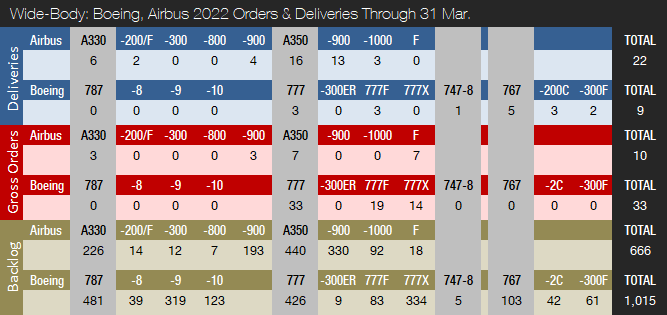

In 2021, Airbus launched the new A350 freighter, or A350F, which is a major and much-needed boost to the company’s competitiveness in the cargo segment. Boeing has long dominated the cargo space with its 737-800BCF, 767-300BCF, 767-300F, 777F, 777-8F and 747-8F offerings. Until now, Airbus has only offered the A330-200F, which has not performed well in competition against Boeing’s popular 767-300F. With the launch of the A350F, it appears Airbus is getting serious about capturing more of the cargo aircraft market. The A350F, which carries up to 120 tons (109 metric tons) of cargo, received its first order in November and will predominantly compete with the 777F. In comparison, the 777F has a cargo capacity of up to 112 tons (102 metric tons). In December 2021, Airbus delivered the 251st and final A380 to Emirates. The A380 is an impressive feat of aeronautical engineering and will, despite its lack of financial success, be forever enshrined in the annals of aviation history. With 123 A380s purchased, Emirates took delivery of nearly half the A380 fleet and currently operates 121 of the superjumbos.

Recently, Airbus urged European leaders to not impose sanctions on titanium imports from Russia. Airbus argues that sanctions on the metal would damage aerospace in Europe while barely hurting the Russian economy. Airbus relies on Russia for half its titanium needs compared to one-third for Boeing. In early March, Boeing said it had suspended Russian titanium purchases. Despite this challenge, Airbus has announced that its titanium sourcing needs are covered in the short and medium-term and recently reaffirmed its 2022 guidance. However, the company is accelerating its search for non-Russian supplies. Both Airbus and Boeing have been stockpiling titanium in recent months.

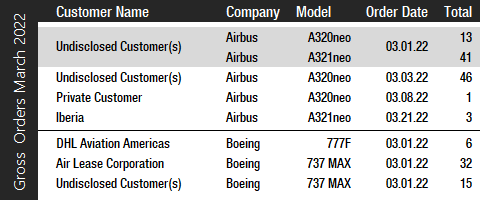

Turning to the March orders review, Boeing had a solid month and booked three orders for a total of 53 jets. The company also reported 15 cancellations (12 737 MAXs and three 787s), resulting in 38 net new orders in total. The largest order was for 32 737 MAXs for Air Lease Corporation (ALC) – a mix of 737-8 and 737-9 jets, followed by an order from an undisclosed customer for 15 737 MAX jets. Finally, DHL decided to boost its freighter fleet and ordered five 777Fs. Year-to-date, Boeing has accumulated 145 net new orders (167 gross orders) compared to 69 net new orders (282 gross orders) in the first quarter last year. In 2021, Boeing booked 909 gross orders and received 430 cancellations, for a total of 479 net new orders (before ASC 606 changes). In 2020, Boeing accumulated a total of 184 gross orders and received 655 cancellations, for a total of -471 net new orders.

Due to events unfolding in Ukraine and sanctions on aircraft deliveries to Russia, Boeing expects that up to 141 jets it has on order – 90 of which are 737 MAX aircraft – could be affected and eventually removed from its books. Please note that for comparison reasons, we do not include these so-called ASC 606 accounting adjustments in the numbers reported in this article and regard net new orders as gross orders minus cancellations.

Following a slow start to 2022, Airbus reported strong bookings in both February and March. In March, the company booked five orders for a total of 104 jets. However, Airbus also reported 76 cancellations (63 A330-900s and 13 A321neos), resulting in only 28 net new orders. AirAsia X, a long-haul budget airline based in Malaysia, canceled 63 of the 78 A330-900 aircraft the airline had on order. The largest order placed in March was for 13 A320neos and 41 A321neos for an undisclosed customer, followed by an order from another undisclosed customer for 46 A320neos. Meanwhile, Iberia ordered three A321neos and a private customer ordered a single A320neo.

Year-to-date, Airbus has accumulated 83 net new orders (253 gross orders) compared to -61 net new orders (39 gross orders) in the first quarter of last year. In 2021, Airbus booked a total of 771 gross orders and received 264 cancellations, for a total of 507 net new orders – enough to win the orders crown for the third year in a row. It should be noted, however, that if Boeing’s 2021 ASC 606 adjustments are included, Boeing comes out ahead with 535 net new orders. In 2020, Airbus accumulated 383 gross orders and received 115 cancellations, for a total of 268 net new orders.

At the end of March 2022, Airbus reported a backlog of 7,023 jets, of which 6,357, or 91 percent, were A220 and A320ceo/neo family narrowbodies. This is 702 aircraft below the company’s all-time backlog record of 7,725 aircraft set in January 2020. By the end of March, Boeing’s backlog (total unfilled orders before ASC 606 adjustment) was 5,186 aircraft, of which 4,171, or 80 percent, were 737 NG/MAX narrowbody jets. Boeing’s all-time backlog high of 5,964 aircraft was set in August 2018. The number of Airbus aircraft to be built and delivered represents 8.1 years of shipments at the 2019 production level (the pre-pandemic level), or 11.5 years based on the 2021 total. In comparison, Boeing’s backlog would “only” last 6.4 years at the 2018 level (the most recent “normal” year for Boeing), or 15.3 years based on 2021 deliveries. In 2022 to date, Boeing’s book-to-bill ratio, calculated as net new orders divided by deliveries, is 1.53. Airbus’ book-to-bill ratio is 0.58. In 2021, Boeing’s book-to-bill ratio was 1.41, while Airbus reported a book-to-bill of 0.81.

2022 Forecast

Forecast International’s Platinum Forecast System is a breakthrough in forecasting technology that provides 15-year production forecasts. The author has used the Platinum Forecast System to retrieve the latest delivery forecast data from the Civil Aircraft Forecast product. For 2022, Forecast International’s analysts currently expect Boeing and Airbus to deliver 455 and 702 commercial jets, respectively. Compared to the 2021 level, this is a 33.8 percent increase for Boeing and a 14.9 percent increase for Airbus.

In January, Boeing reported Q4 and full-year 2021 earnings and operating results but did not provide any guidance on expected 2022 deliveries. The company will release first quarter results on April 27. Airbus reported 2021 earnings on February 17 and expects to deliver 720 commercial aircraft in 2022. As the basis for its 2022 guidance, Airbus assumes no further disruptions to the world economy, air traffic, and its own internal operations. The company recently reaffirmed its 2022 guidance and expects to release Q1 2022 earnings on May 4.

References:

- https://www.forecastinternational.com/platinum.cfm

- http://www.boeing.com/commercial/#/orders-deliveries

- https://www.airbus.com/aircraft/market/orders-deliveries.html

- https://boeing.mediaroom.com/2022-04-04-Air-Lease-Corporation-Adds-32-Boeing-737-MAX-Jets-to-Its-Orderbook

- https://www.reuters.com/business/aerospace-defense/exclusive-boeing-tests-suppliers-787-output-hikes-sources-2022-03-11/

- https://www.reuters.com/business/aerospace-defense/airbus-accelerates-hunt-alternative-titanium-supplies-2022-04-12/

- https://www.reuters.com/business/aerospace-defense/boeing-suspends-part-its-business-russia-wsj-2022-03-07/

- https://edition.cnn.com/2022/04/12/business/boeing-lost-orders/index.html

- https://edition.cnn.com/2022/03/27/business/boeing-china-problems/index.html

- https://boeing.mediaroom.com/2022-01-31-Boeing-Launches-777-8-Freighter-to-Serve-Growing-Demand-for-Cargo,-Enhanced-Environmental-Performance

- https://www.reuters.com/business/aerospace-defense/exclusive-boeing-aims-nearly-double-737-max-production-by-end-2023-sources-2022-03-05/

Forecast International’s Civil Aircraft Forecast covers the rivalry between Airbus and Boeing in the large airliner sector; the emergence of new players in the regional aircraft segment looking to compete with Bombardier, Embraer, and ATR; and the shifting dynamics within the business jet market as aircraft such as the Bombardier Global 7000, Cessna Hemisphere, and Gulfstream G600 enter service. Also detailed in this service are the various market factors propelling the general aviation/utility segment as Textron Aviation, Cirrus, Diamond, Piper, and a host of others battle for sales and market share. An annual subscription includes 75 individual reports, most with a 10-year unit production forecast. Click here to learn more.

Kasper Oestergaard is an expert in aerospace & defense market intelligence, fuel efficiency in civil aviation, defense spending and defense programs. Mr. Oestergaard has a Master's Degree in Finance and International Business from the Aarhus School of Business - Aarhus University in Denmark. He has written four aerospace & defense market intelligence books as well as numerous articles and white papers about European aerospace & defense topics.