Strong comeback for 737 MAX deliveries /// Boeing 6,000+ aircraft backlog record in sight

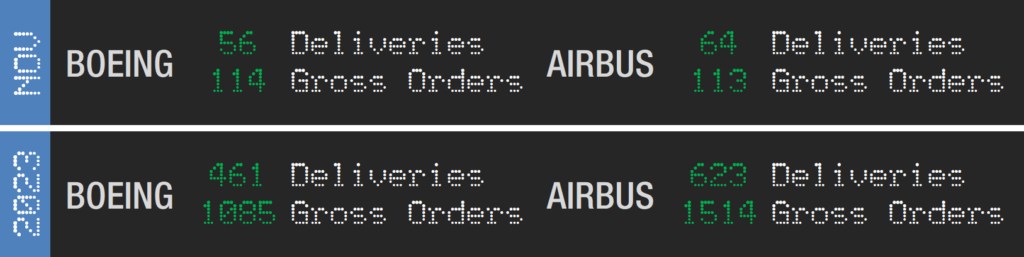

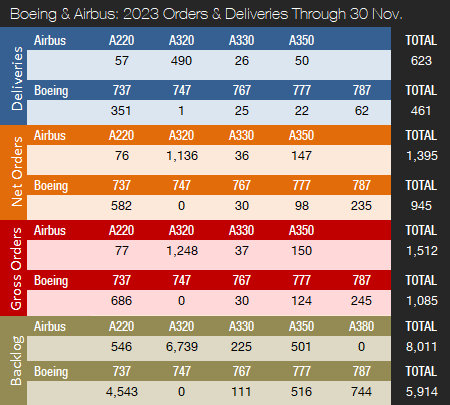

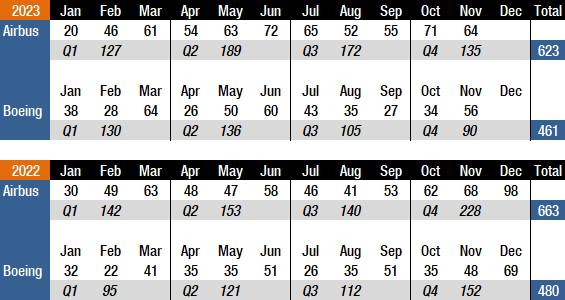

Boeing and Airbus delivered 56 and 64 commercial jets in November 2023, compared to 48 and 68 deliveries, respectively, in the same month last year. Year-to-date, Boeing and Airbus have delivered 461 and 623 aircraft compared to 411 and 565, respectively, during the first eleven months of 2022. As of November, Boeing and Airbus are 50 and 58 deliveries ahead of last year’s totals to date. In 2022, Airbus won the deliveries crown for the fourth year in a row by delivering 663 aircraft, compared to Boeing’s 480 shipments.

Following a more than challenging 2020 due to the COVID-19 pandemic, 2021 and 2022 were recovery years for the two largest commercial plane makers. This year has been another year of recovery for the commercial aircraft manufacturing industry. However, Boeing and Airbus still have quite a way to go before deliveries are back to pre-pandemic levels. In 2018, before COVID-19 and the 737 MAX grounding, Boeing delivered 806 jets, a level that will likely not be recaptured before the 2025-26 timeframe. Airbus’ record high of 863 shipments was set in 2019, a level that could be surpassed in 2024 if the supply chain can keep up, but most likely not before 2025. Also, Airbus is expected to retain the deliveries lead for the foreseeable future due to the company’s comfortable backlog lead over its American rival. Before 2019, Boeing had out-delivered Airbus every year since 2012.

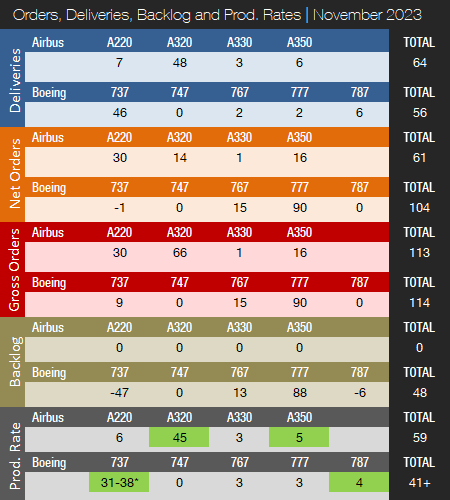

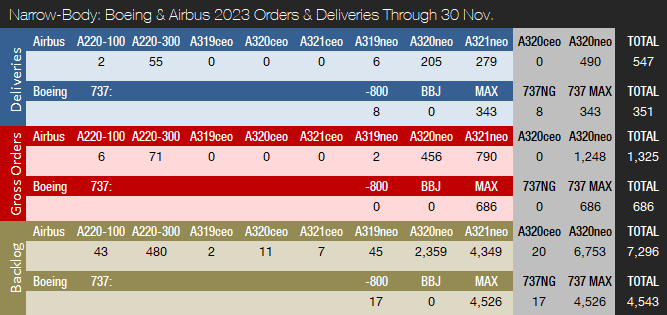

As indicated above, in November 2023, Boeing delivered 56 jets, including 45 737s (44 MAXs / 1 NG), two 767s, two 777s, and six 787s. Boeing’s numbers came roaring back in November thanks to strong 737 MAX shipments. The 737 MAX program had some catching up to do after a manufacturing issue discovered in August this year negatively impacted aircraft deliveries for several months. The 737 program continues to transition production to 38 jets per month. Since June of last year, the 737 program has been producing aircraft at an official rate of 31 per month and, year-to-date, Boeing has now delivered 32 jets per month, on average. At their Q3 earnings call, Boeing announced that they expect the transition to be completed by the end of the year. At the same time, Boeing reduced its guidance from 400-450 737 MAX deliveries for the year to 375-400, due to required rework to remedy the aforementioned 737 MAX production defect. With 343 737 MAXs delivered to date, this means that Boeing expects to deliver 32-57 MAXs in December. In the long term, Boeing expects to increase production to approximately 50 jets per month in the 2025/26 timeframe. This compares to the pre-crash/pre-pandemic rate of 52 737s per month in 2018. Recently, it was reported that the company is planning to boost production to 52 jets per month by January 2025. The company plans to open a new 737 MAX production line in Everett in the second half of 2024. The new line is in addition to the three lines currently in place in Renton. Boeing ended the second quarter with 250 737 MAX jets in inventory, up 22 from Q2 2023. Customers in China account for 85 of these aircraft. Boeing expects most of the inventoried jets will be delivered by the end of 2024. The company is still producing 737 NGs but only has 17 737-800s remaining in backlog.

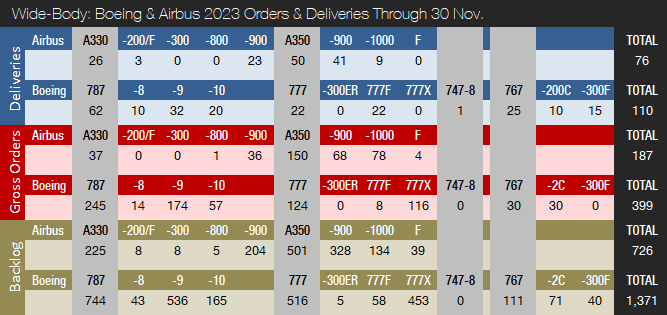

In August of last year, deliveries of the Boeing 787 Dreamliner were resumed following a suspension of shipments that lasted nearly 16 months. Boeing had suspended Dreamliner deliveries in May 2021 for the second time in less than a year. At the end of June, the 787 production rate was raised for the second time this year and is now four per month. The 787 program is currently transitioning to a rate of five per month (for a total of 70-80 deliveries for the year), followed by further increases before reaching 10 aircraft per month by 2025/26. Boeing ended the first quarter with 75 Dreamliners in inventory, down 10 from Q2 2023. Most of these aircraft will be delivered during 2023 and 2024.

The 747 program closed down production when the last aircraft was delivered to Atlas Air in January this year. The 767 program is currently producing at a rate of three units per month, a mix of KC-46 tankers (based on the 767-2C) and 767-300 freighters. The 777 program is currently pushing out aircraft at a rate of three per month. Most aircraft in backlog are 777 freighters, with only five 777-300ERs left. The 777 program was expected to get a new addition in late 2023 with the first delivery of the 777X, but in April of last year, Boeing announced this will now not happen before 2025. This reflects an updated assessment of the time required to meet certification requirements. Last year, Boeing launched a new 777X-based freighter, thereby expanding its 777X and cargo portfolio. By the 2025/26 timeframe, Boeing expects to be delivering four 777s per month.

In November 2023, Airbus delivered 64 jets, including seven A220s, 48 A320s (all NEO), three A330s, and six A350s. The official A320 production rate is 45 aircraft per month and has remained at this level since the end of 2021. On average, the company has delivered 45 A320s per month in 2023 compared to 43 in 2022. Production is currently being increased and an official rate hike can be expected soon. The A320 program is expected to reach a monthly rate of 65 by late 2024 (pushed back twice now due to supply chain challenges). Also, Airbus is working with its supply chain to increase A320 production to 75 aircraft per month in 2026. The A321XLR flight test program is reportedly progressing well, and entry into service is expected to take place in the second quarter of 2024.

The A220, meanwhile, is being produced at a rate of six aircraft per month, with a monthly production rate of 14 expected by 2025. Airbus is currently planning to launch a stretch version of the A220, which many now refer to as the “A220-500” or even “A221.” Currently, the Pratt & Whitney PW1500G is the only engine option for the A220, and the new variant will most likely come with a second engine option.

The A330 production rate was increased from two aircraft per month to three at the end of 2022, with an increase to four per month expected in 2024. The A350 production rate currently averages five per month and was expected to be increased to six by early 2023. However, the rate increase has been pushed back to late 2023. Airbus expects to produce nine A350s per month by 2025.

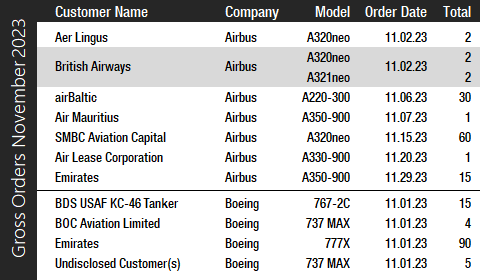

Turning to the November orders review, Boeing had a solid month thanks to Dubai Airshow, however, many orders placed at the show have not yet been booked. The company booked orders from four customers for a total of 114 jets (gross orders) and reported 10 737 MAX cancellations, resulting in 104 net new orders. The November orders haul was dominated by Emirates’ large Dubai order for 90 777X jets, comprised of 35 777-8s and 55 777-9s. The order is a major vote of confidence in Boeing’s largest commercial jet and, with 453 777Xs now in backlog, Boeing can feel more at ease. Also in November, the U.S. Air Force placed an order for another 15 KC-46 tankers (based on the 767-2C), while BOC Aviation and an undisclosed customer ordered a total of nine 737 MAXs. Year-to-date, Boeing has accumulated 945 net new orders (1,085 gross orders), compared to 571 net new orders (685 gross orders) in the first eleven months of last year. In 2022, Boeing booked 774 net new orders (935 gross orders) before ASC 606 changes. Please note that for comparison reasons, we do not include Boeing’s so-called ASC 606 accounting adjustments in the numbers reported in this article and regard net new orders as gross orders minus cancellations.

In November, despite a somewhat disappointing orders haul in Dubai, Airbus had a good month and booked orders for 113 aircraft from seven different customers and reported 52 cancellations (50 A320neo and two A321neo), for a total of 61 net new orders. Ireland-based SMBC Aviation Capital, one of the world’s largest aircraft leasing firms, placed a large order for 60 A320neos, while airBaltic and Emirates – in Dubai – booked 30 A220-300s and 15 A350-900s, respectively. Year-to-date, Airbus has accumulated 1,395 net new orders (1,512 gross orders), compared to 810 net new orders (1,062 gross orders) in the first eleven months of 2022. In 2022, Airbus booked 820 net new orders (1,078 gross orders). In 2022, Airbus won the orders crown for the fourth consecutive year by a fairly slim margin of just 46 aircraft compared to Boeing.

At the end of November, Airbus reported a backlog of 8,011 jets, of which 7,285, or 91 percent, were A220 and A320ceo/neo family narrowbodies. Airbus’ all-time backlog record was set in August this year when the company reported a backlog of 8,024 jets, surpassing the old record of 7,967 jets set in June this year just after Paris Air Show. By the end of last month, Boeing’s backlog (total unfilled orders before ASC 606 adjustment) was 5,914 aircraft, of which 4,543, or 77 percent, were 737 NG/MAX narrowbody jets. Boeing’s all-time backlog high of 5,964 aircraft was set in August 2018, and the company is looking set to surpass this figure when all Dubai Airshow orders are included in the near future. If Boeing had included all their firm Dubai orders at the end of November, the company would have set a new all-time backlog record high of 6,038 jets.

![]()

We had expected a new backlog record this month, however, Boeing is likely waiting for next month’s update to make a big splash when full-year 2023 numbers are released. While well behind Airbus’ backlog, Boeing has increased its order book significantly in recent years and is expected to continue to set new records in 2024 and beyond. The number of Airbus aircraft to be built and delivered represents 9.3 years of shipments at the 2019 production level (the pre-pandemic level), or 12.1 years based on the 2022 total. In comparison, Boeing’s backlog would “only” last 7.3 years at the 2018 level (the most recent “normal” year for Boeing), or 12.3 years based on 2022 deliveries. As of November 30, Boeing’s book-to-bill ratio this year, calculated as net new orders divided by deliveries, is a very strong 2.05 with Airbus coming in even higher at 2.24. This means that both companies have received more than two new firm orders for every aircraft the company has delivered so far this year. In 2022, Boeing’s book-to-bill ratio was a very strong 1.61. Meanwhile, Airbus’ book-to-bill ratio was a solid 1.24.

2023 Forecast

Forecast International’s Platinum Forecast System is a breakthrough in forecasting technology that provides 15-year production forecasts. The author has used the Platinum Forecast System to retrieve the latest delivery forecast data from the Civil Aircraft Forecast product. For 2023, Forecast International’s analysts currently expect Boeing and Airbus to deliver 513 and 704 commercial jets, respectively. Please note that these figures exclude militarized variants of commercial platforms such as Boeing’s P-8 Poseidon maritime patrol aircraft and KC-46 Pegasus tanker and Airbus’ A330 MRTT tanker.

Boeing released Q3 2023 results on October 25 and lowered its 2023 guidance for 737 MAX deliveries from 400-450 to 375-400 due to the aforementioned production issue concerning the aft pressure bulkhead. Near-term deliveries and production will be impacted as the company performs necessary inspections and rework. Boeing reaffirmed its 787 guidance from November of last year calling for 70-80 deliveries in total. Airbus released its 9M 2023 results on November 8 and reaffirmed the previous guidance for 720 commercial jet deliveries in 2023.

Note: Light green color for production rates means the program is currently transitioning to a higher rate.

*Boeing is currently transitioning from 31 to 38 737 MAXs per month. The official rate is still 31/mo.

References:

- https://www.forecastinternational.com/platinum.cfm

- http://www.boeing.com/commercial/#/orders-deliveries

- https://www.airbus.com/aircraft/market/orders-deliveries.html

- https://boeing.mediaroom.com/2023-10-25-Boeing-Reports-Third-Quarter-Results

- https://www.airbus.com/en/newsroom/press-releases/2023-11-airbus-reports-nine-month-9m-2023-results

- https://www.airbus.com/en/newsroom/press-releases/2023-11-smbc-aviation-capital-orders-60-a320neo-family-aircraft

Kasper Oestergaard is an expert in aerospace & defense market intelligence, fuel efficiency in civil aviation, defense spending and defense programs. Mr. Oestergaard has a Master's Degree in Finance and International Business from the Aarhus School of Business - Aarhus University in Denmark. He has written four aerospace & defense market intelligence books as well as numerous articles and white papers about European aerospace & defense topics.