April orders very low. Boeing 737 MAX deliveries impacted by Spirit manufacturing issue.

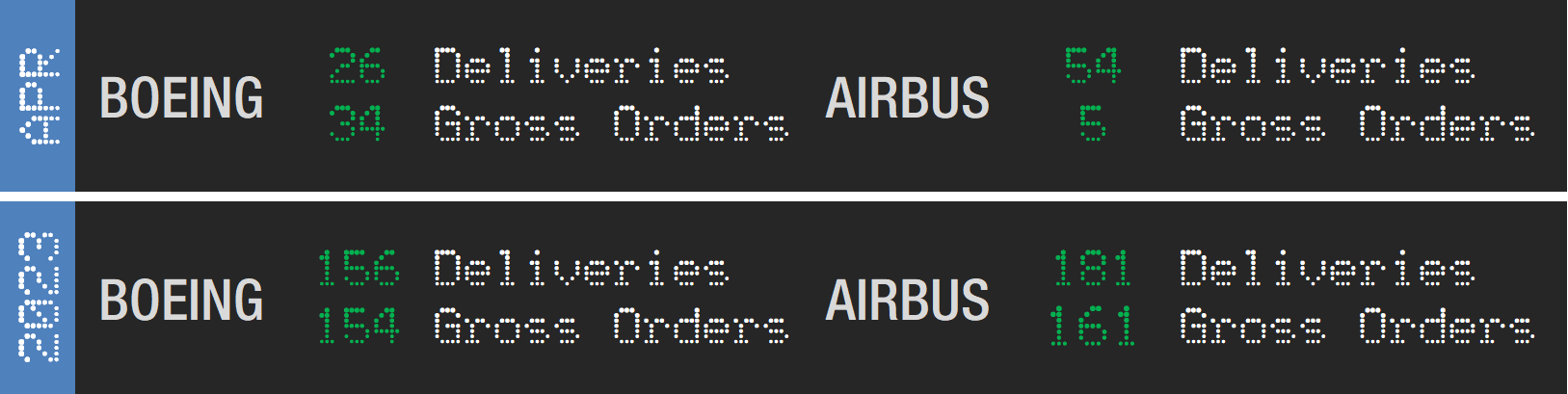

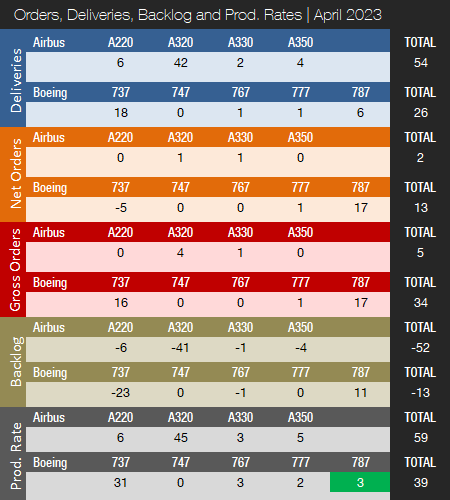

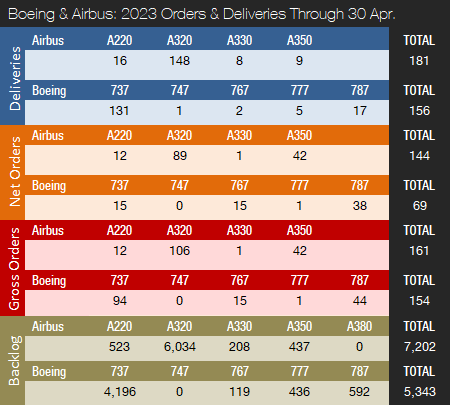

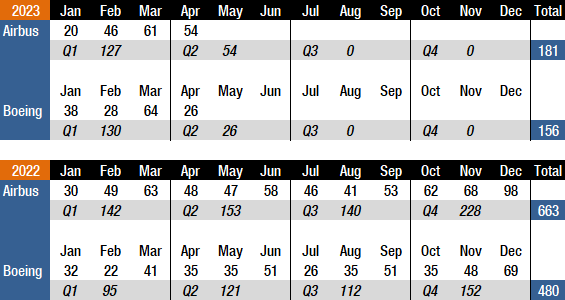

Boeing and Airbus delivered 26 and 54 commercial jets in April 2023, compared to 35 and 48 deliveries, respectively, in the same month last year. Boeing’s April delivery figures were impacted by a manufacturing issue that was discovered recently and affects a significant number of undelivered 737 MAX airplanes, both in production and in storage. Year-to-date, Boeing and Airbus have delivered 156 and 181 aircraft, compared to 130 and 190, respectively, for the first four months of 2022. After the first four months of the year, Boeing is 26 deliveries ahead of, and Airbus is nine deliveries behind, last year’s totals to date. In 2022, Airbus won the deliveries crown for the fourth year in a row by delivering 663 aircraft, compared to Boeing’s 480 shipments. In 2021, Boeing and Airbus delivered 340 and 611 aircraft.

Following a more-than-challenging 2020 due to the COVID-19 pandemic, 2021 and 2022 were recovery years for the two largest commercial plane makers. Another year of recovery for the commercial aircraft manufacturing industry can be expected in 2023 despite ongoing supply chain challenges, inflation and higher interest rates, labor shortages, and the war in Ukraine. However, Boeing and Airbus still have quite a way to go before deliveries are back to pre-pandemic levels. In 2018, before COVID-19 and the 737 MAX grounding, Boeing delivered 806 jets, a level that will likely not be recaptured before the 2025-26 timeframe. Airbus’ all-time record high of 863 shipments was set in 2019, a level that could be surpassed in 2024 if supply chain challenges ease, but most likely not before 2025. Also, Airbus is expected to retain the deliveries lead for the foreseeable future due to the company’s comfortable backlog lead over its American rival. Prior to 2019, Boeing had out-delivered Airbus every year since 2012.

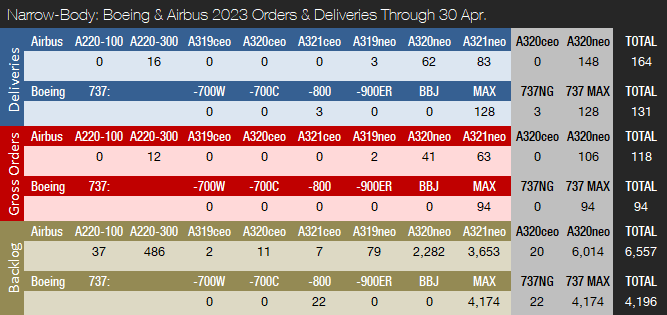

As indicated above, in April 2023, Boeing delivered 26 jets, including 18 737s (17 MAXs and one NG), one 767, one 777, and six 787s. Since June of last year, the 737 program has been producing aircraft at an official rate of 31 per month. The monthly production trend is expected to remain in the low 30s for now, but will be increased as soon as the supply chain allows. For 2023, Boeing targets an average rate of between 33 and 38 737s per month, or 400-450 for the year. Due to very strong 737 MAX deliveries in March, Boeing delivered 38 737s per month, on average, in the first quarter of the year; however, this figure includes aircraft from inventory. Longer term, Boeing expects to increase production to approximately 50 jets per month in the 2025/26 timeframe. This compares to the pre-crash/pre-pandemic rate of 52 737s per month in 2018. Recently, it was reported that the company is planning to boost production to 52 jets per month by January 2025. The company plans to open a fourth 737 MAX production line in Renton in the second half of 2024. Boeing ended the first quarter with 225 737 MAX jets in inventory, down 25 from Q4 2022. Customers in China account for 138 of these aircraft. Boeing expects most of the inventoried jets will be delivered by the end of 2024. At present, Boeing’s main supply chain headache is its engine supply. Boeing expects that supply chain constraints will remain a significant challenge in 2023. The company is still producing 737 NGs, but only has 22 737-800s remaining in backlog.

On April 14, Boeing announced that a manufacturing issue affecting a significant number of undelivered 737 MAX airplanes, both in production and in storage, has been discovered. The company stressed that the problem is not an immediate safety of flight issue and that the in-service fleet can continue operating safely. As mentioned above, Spirit AeroSystems, which produces the 737’s fuselage, reportedly used a non-standard manufacturing process during the installation of two fittings in the rear fuselage. Spirit AeroSystems is working to develop an inspection and rework plan for the affected fuselages. The work will impact deliveries over the next several months. However, Boeing still expects to deliver 450 737 airplanes this year. Within the 225 inventoried 737 MAX airplanes, roughly 75 percent will require fuselage rework.

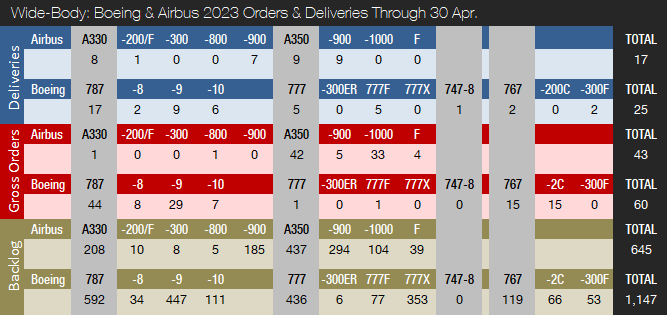

In August of last year, deliveries of the Boeing 787 Dreamliner were resumed following a suspension of shipments that lasted nearly 16 months. Boeing had suspended Dreamliner deliveries in May 2021 for the second time in less than a year. The 787 production rate was recently raised to three aircraft per month, up from two. The 787 rate will return to five per month by the end of 2023 (for a total of 70-80 deliveries for the year), followed by further increases before reaching 10 aircraft per month by 2025/26. Boeing ended the first quarter with 95 Dreamliners in inventory, down five from Q4 2022. Most of these aircraft will be delivered during 2023 and 2024.

The 747 program closed down production when the last aircraft was delivered to Atlas Air on January 31 (note: for some reason, this aircraft was still on Boeing’s books at the end of January but was removed in February). The 767 program is currently producing at a rate of three units per month, a mix of KC-46 tankers (based on the 767-2C) and 767-300 freighters. The 777 program is currently pushing out aircraft at a rate of two per month. Most aircraft in backlog are 777 freighters, with only six 777-300ERs left. The 777 program was expected to get a new addition in late 2023 with the first delivery of the 777X, but in April of last year Boeing announced this will now not happen before 2025. This reflects an updated assessment of the time required to meet certification requirements. Last year, Boeing launched a new 777X-based freighter, thereby expanding its 777X and cargo portfolio. By the 2025/26 timeframe, Boeing expects to be delivering four 777s per month.

In April 2023, Airbus delivered 54 jets, including six A220s, 42 A320s (all NEO), two A330s, and four A350s. The official A320 production rate is 45 aircraft per month and has remained at this level since the end of 2021. On average, the company delivered 43 A320s per month in 2022 but has only delivered 37 per month during the first four months of this year. Current plans call for production to be increased later this year until reaching a monthly rate of 65 by late 2024 (pushed back twice now due to supply chain challenges). Also, Airbus is working with its supply chain to increase A320 production to 75 aircraft per month in 2026. It was recently announced that Airbus plans to add a second A320 final assembly line in Tianjin, China. The A321XLR flight test program is reportedly progressing well, and entry into service is expected to take place in the second quarter of 2024.

The A220, meanwhile, is being produced at a rate of six aircraft per month, with a monthly production rate of 14 expected by 2025. The A350 production rate currently averages five per month and was expected to be increased to six by early 2023. However, the rate increase is likely to be pushed back to late 2023. Airbus expects to produce nine A350s per month by 2025. The A330 production rate was increased from two aircraft per month to three at the end of 2022, with an increase to four per month expected in 2024.

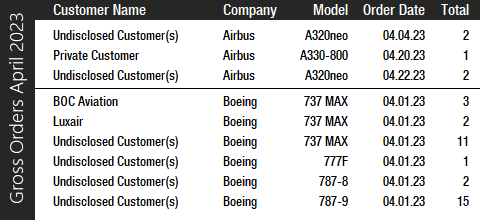

Turning to the April orders review, Boeing had a somewhat quiet month and booked orders from six customers for a total of 34 jets (gross orders). However, the company also reported 21 cancellations (all 737 MAXs), resulting in just 13 net new orders. The 787 was in demand in March (20 orders) and again this month with 17 aircraft added to Boeing’s books, including 15 787-9s and two 787-8s for undisclosed customers. Also in April, BOC Aviation, Luxair and an undisclosed customer ordered a total of 16 737 MAX jets. Finally, an undisclosed customer ordered a single 777F. Year-to-date, Boeing has accumulated 69 net new orders (154 gross orders), compared to 157 net new orders (213 gross orders) in the first four months of last year. In 2022, Boeing booked 774 net new orders (935 gross orders), up from 479 net new orders (909 gross orders) in 2021 (before ASC 606 changes). Please note that for comparison reasons, we do not include Boeing’s so-called ASC 606 accounting adjustments in the numbers reported in this article and regard net new orders as gross orders minus cancellations.

In April, Airbus had a very quiet month and booked orders for just five aircraft from three different customers and reported three A320neo cancellations, for a total of two net new orders. Two undisclosed customers each ordered two A320neos, while a private customer booked a single A330-800. Year-to-date, Airbus has accumulated 144 net new orders (161 gross orders), compared to 178 net new orders (351 gross orders) in the four months of last year. In 2022, Airbus booked 820 net new orders (1,078 gross orders), surpassing both 2021 gross orders and net new orders. In 2022, Airbus won the orders crown for the fourth consecutive year by a fairly slim margin of just 46 aircraft compared to Boeing. In 2021, Airbus booked a total of 771 gross orders and received 264 cancellations, for a total of 507 net new orders.

At the end of April, Airbus reported a backlog of 7,202 jets, of which 6,557, or 91 percent, were A220 and A320ceo/neo family narrowbodies. This is 523 aircraft below the company’s all-time backlog record of 7,725 aircraft set in January 2020. By the end of last month, Boeing’s backlog (total unfilled orders before ASC 606 adjustment) was 5,343 aircraft, of which 4,196, or 79 percent, were 737 NG/MAX narrowbody jets. Boeing’s all-time backlog high of 5,964 aircraft was set in August 2018. The number of Airbus aircraft to be built and delivered represents 8.3 years of shipments at the 2019 production level (the pre-pandemic level), or 10.9 years based on the 2022 total. In comparison, Boeing’s backlog would “only” last 6.6 years at the 2018 level (the most recent “normal” year for Boeing), or 11.1 years based on 2022 deliveries. As of April 30, Boeing’s book-to-bill ratio this year, calculated as net new orders divided by deliveries, is 0.44, compared to Airbus at 0.80. This means that both companies are currently tapping into their backlog. In 2022, Boeing’s book-to-bill ratio was a very strong 1.61. Meanwhile, Airbus’ book-to-bill ratio was a solid 1.24.

2023 Forecast

Forecast International’s Platinum Forecast System is a breakthrough in forecasting technology that provides 15-year production forecasts. The author has used the Platinum Forecast System to retrieve the latest delivery forecast data from the Civil Aircraft Forecast product. For 2023, Forecast International’s analysts currently expect Boeing and Airbus to deliver 500 and 710 commercial jets, respectively. Please note that these figures exclude militarized variants of commercial platforms such as Boeing’s P-8 Poseidon maritime patrol aircraft and KC-46 Pegasus tanker and Airbus’ A330 MRTT tanker.

Boeing released its Q1 2023 results on April 26 and reaffirmed its 2023 737 MAX and 787 guidance from November of last year. On the investor earnings call, CEO David Calhoun stated, “We still expect to deliver 450 737 airplanes this year.” In November of last year, Boeing announced that it expects to deliver 400-450 737s and 70-80 787s in 2023, which equates to a monthly average of 33-38 for the 737. Meanwhile, Airbus is targeting 720 commercial jet deliveries in 2023. The company reported its first quarter 2023 results on May 3 and reaffirmed its guidance.

References:

- https://www.forecastinternational.com/platinum.cfm

- http://www.boeing.com/commercial/#/orders-deliveries

- https://www.airbus.com/aircraft/market/orders-deliveries.html

- https://boeing.mediaroom.com/2023-04-26-Boeing-Reports-First-Quarter-Results

- https://seekingalpha.com/article/4596854-boeing-company-ba-q1-2023-earnings-call-transcript

- https://seekingalpha.com/article/4572364-boeing-company-ba-q4-2022-earnings-call-transcript

- https://www.spiritaero.com/pages/release/spirit-aerosystems-statement-on-737/

- https://boeing.mediaroom.com/2023-04-11-Boeing-Announces-First-Quarter-Deliveries

- https://edition.cnn.com/2023/04/14/business/boeing-737-max-problems/index.html

- https://simpleflying.com/boeing-737-max-deliveries-delayed-spirit-aerosystems-mistake/

- https://www.airbus.com/en/newsroom/press-releases/2023-05-airbus-reports-first-quarter-q1-2023-results

Kasper Oestergaard is an expert in aerospace & defense market intelligence, fuel efficiency in civil aviation, defense spending and defense programs. Mr. Oestergaard has a Master's Degree in Finance and International Business from the Aarhus School of Business - Aarhus University in Denmark. He has written four aerospace & defense market intelligence books as well as numerous articles and white papers about European aerospace & defense topics.