Year of Recovery Continues for Commercial Jet Makers – 737-10 Successfully Completes First Flight

by J. Kasper Oestergaard, European Correspondent, Forecast International.

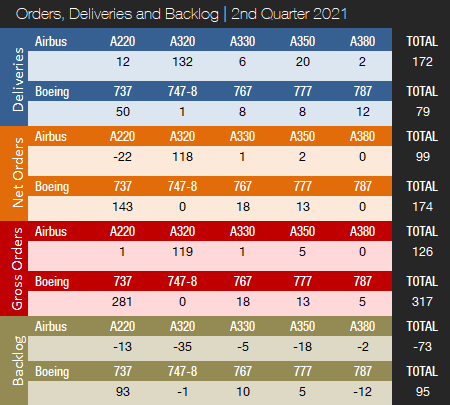

Boeing and Airbus delivered 79 and 172 commercial jets in the second quarter of 2021, compared to 20 and 74 deliveries, respectively, in Q2 2020. For the full year 2020, Boeing delivered 157 aircraft, compared to 380 and 806 in 2019 and 2018, respectively. In 2020, Airbus delivered 566 aircraft and won the deliveries crown for the second year in a row. Due to COVID-19, deliveries were down from 863 and 800 in 2019 and 2018, respectively. Airbus is expected to retain the deliveries crown for years to come due to the company’s comfortable backlog lead over its American rival. Prior to 2019, Boeing had out-delivered Airbus every year since 2012.

Following a more than challenging 2020 due to the COVID-19 pandemic, 2021 is on track to be a year of recovery for the two largest commercial plane makers. The past two years have particularly been challenging for Boeing, but things are now looking brighter. Orders and deliveries are on the rise and the 737 MAX has been cleared to return to the skies in much of the world. However, China, the world’s second-largest market for commercial air traffic, is still prohibiting the plane from flying. But Chinese aviation officials recently expressed willingness to conduct flight tests on the aircraft. Boeing reportedly plans to send a team of 35 pilots and engineers to China to meet officials in late July.

In Q2 2021, Boeing delivered 79 jets – up from 77 in Q1 – including 50 737s (47 MAX / 3 NG), one 747-8, eight 767s, eight 777s, and 12 787s. Production of the 737 MAX was suspended from January 2020 until the end of May of that year, when Boeing announced it had commenced low-rate production of the aircraft. Boeing continues to expect the 737 MAX production rate to gradually increase to 31 per month by early 2022, with further increases as market demand allows. Meanwhile, Boeing had reduced the 787 production rate from 14 per month (rate at the start of 2020) to just five per month as of March 2021. Boeing has now moved all 787 final assembly to its facilities in Charleston, South Carolina. Boeing resumed 787 deliveries in late March, following comprehensive reviews to ensure the aircraft meets company standards.

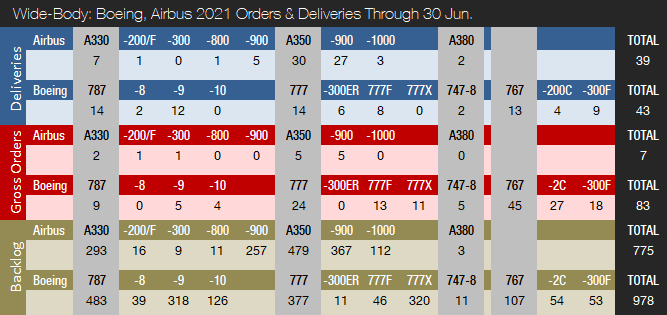

In Q2 2021, Airbus delivered 172 jets (up from 125 in Q1), including 12 A220s, 132 A320s (125 NEO / 7 CEO), six A330s, 20 A350s, and two A380s. Prior to the pandemic, Airbus was targeting a 5 percent A320 rate increase to 63 jets per month from 2021, and was also discussing a further ramp-up with its supply chain that could have brought the production rate up to as high as 67 aircraft per month, or 804 per year, by 2023. This would have put the company within reach of a total of 1,000 jet deliveries per year. These plans have now been shelved. In January 2021, Airbus released an updated production rate plan and now expects to increase A320 production from the current rate of 40 per month to 43 in Q3 and 45 in Q4 2021. This represents a slower ramp-up than the previously anticipated 47 aircraft per month from July. The A220 monthly production rate was increased from four to five aircraft per month by the end of Q1 2021. Widebody production rates will remain at current levels, with monthly production rates of around five and two for the A350 and A330, respectively. With only three A380s in backlog as of June 30, 2021, the end of the A380 program draws near. The last aircraft is expected to be delivered to Emirates in May 2022.

Turning to the Q2 2021 orders race, Boeing had a strong quarter and booked 12 orders for a total of 317 jets; however, the company also reported 143 cancellations, of which 138 were for the 737 MAX. The 317 gross orders included 281 737s (all MAX), 18 767s, 13 777s, and five 787s. The largest order was for 200 737 MAX narrowbodies for United Airlines, including 150 737-10s and 50 737-8s. The purchase increases the airline’s 737 MAX order book to 380 aircraft, excluding the 30 aircraft that have been delivered to United to date. As the launch customer for the 737-10, United placed its first order in 2017 by converting 100 737-9 orders to the larger 737-10 variant. Also in Q2 2021, Southwest Airlines ordered 34 Boeing 737 MAX 7s. In 2020, Boeing accumulated a total of 184 gross orders and received 655 cancellations, for a total of -471 net new orders.

In Q2 2021, Airbus booked seven new orders for a total of 126 jets and reported 27 cancellations. Orders included a single A220, 119 A320s (all NEO), one A330, and five A350s. The largest order was United Airlines’ order for 70 A321neos. Other significant bookings were Delta Air Lines’ order for 25 A321neos and Avolon’s order for 22 A320neos (14 A320neo / 8 A321neo). In 2020, Airbus accumulated 383 gross orders and received 115 cancellations, for a total of 268 net new orders – enough to win the orders crown for the second year in a row.

At the end of June, Airbus reported a backlog of 6,925 jets, of which 6,150, or 89 percent, were A220 and A320ceo/neo family narrowbodies. This is 800 aircraft below the company’s all-time backlog record of 7,725 aircraft set in January 2020. By the end of June 2021, Boeing’s backlog (total unfilled orders before ASC 606 adjustment) was 5,084 aircraft, of which 4,106, or 81 percent, were 737 NG/MAX narrowbody jets. Boeing’s all-time backlog high of 5,964 aircraft was set in August 2018. The number of Airbus aircraft to be built and delivered represents 8.0 years of shipments at the 2019 production level, or 12.2 years based on the 2020 total. In comparison, Boeing’s backlog would “only” last 6.3 years at the 2018 level (the most recent “normal” year for Boeing), 13.4 years based on 2019 production totals, and 32.4 years at the extremely low 2020 total, which the company will easily surpass in 2021. In 2021, Boeing’s book-to-bill ratio, calculated as net new orders divided by deliveries, is 1.56, ahead of Airbus’ book-to-bill ratio of 0.13. In 2020, Boeing’s book-to-bill ratio was negative, while Airbus reported a book-to-bill of 0.47.

2021 Forecast

Forecast International’s Platinum Forecast System is a breakthrough in forecasting technology that provides 15-year production forecasts. The author has used the Platinum Forecast System to retrieve the latest delivery forecasts and, for 2021, Forecast International’s analysts currently expect Boeing and Airbus to deliver 339 and 583 commercial jets, respectively.

When releasing its Q1 2021 earnings in April 2021, Airbus announced that it expects to deliver the same number of commercial aircraft as in 2020 (566 aircraft). The company reiterated the guidance when releasing its first quarter earnings report in April 2021. Boeing has not provided any guidance regarding the quantity of aircraft it expects to deliver this year.

On July 28, Boeing will report Q2 2021 earnings and operating results, to be followed by Airbus’ report the day after.

References:

- https://www.forecastinternational.com/platinum.cfm

- http://www.boeing.com/commercial/#/orders-deliveries

- https://www.airbus.com/aircraft/market/orders-deliveries.html

- https://boeing.mediaroom.com/2021-04-28-Boeing-Reports-First-Quarter-Results

- https://boeing.mediaroom.com/2021-06-18-Boeing-Completes-Successful-737-10-First-Flight

- https://boeing.mediaroom.com/United-Airlines-Orders-200-More-Boeing-737-MAX-Jets

- https://www.reuters.com/business/aerospace-defense/china-open-boeing-737-max-test-flights-bloomberg-news-2021-07-08/

Forecast International’s Civil Aircraft Forecast covers the rivalry between Airbus and Boeing in the large airliner sector; the emergence of new players in the regional aircraft segment looking to compete with Bombardier, Embraer, and ATR; and the shifting dynamics within the business jet market as aircraft such as the Bombardier Global 7000, Cessna Hemisphere, and Gulfstream G600 enter service. Also detailed in this service are the various market factors propelling the general aviation/utility segment as Textron Aviation, Cirrus, Diamond, Piper, and a host of others battle for sales and market share. An annual subscription includes 75 individual reports, most with a 10-year unit production forecast. Click here to learn more.

Based in Denmark, Joakim Kasper Oestergaard is Forecast International’s AeroWeb Webmaster and European Editor. In 2008, he came up with the idea for what would eventually evolve into AeroWeb. Mr. Oestergaard is an expert in aerospace & defense market intelligence, fuel efficiency in civil aviation, defense spending and defense programs. He has an affiliation with Terma Aerostructures A/S in Denmark – a leading manufacturer of composite and metal aerostructures for the F-35 Lightning II. Mr. Oestergaard has a Master’s Degree in Finance and International Business from the Aarhus School of Business – Aarhus University in Denmark.

For more than 50 years, Forecast International intelligence reports have been the aerospace and defense industry standard for accurate research, analysis, and projections. Our experienced analysts compile, evaluate, and present accurate data for decision makers. FI's market research reports offer concise analysis of individual programs and identify market opportunities. Each report includes a program overview, detailed statistics, recent developments and a competitive analysis, culminating in production forecasts spanning 10 or 15 years. Let our market intelligence reports be a key part of reducing uncertainties and mastering your specific market and its growth potential. Find out more at www.forecastinternational.com