Narrowbody Production Remains Steady /// Delivery Cadence Improves From January /// Boeing to Outdeliver Airbus For Second Consecutive Month

For the purposes of this article, Forecast International considers an aircraft to be “produced” once it completes its first test flight, and “delivered” when it is contractually handed over to the customer.

Production by Market Segment

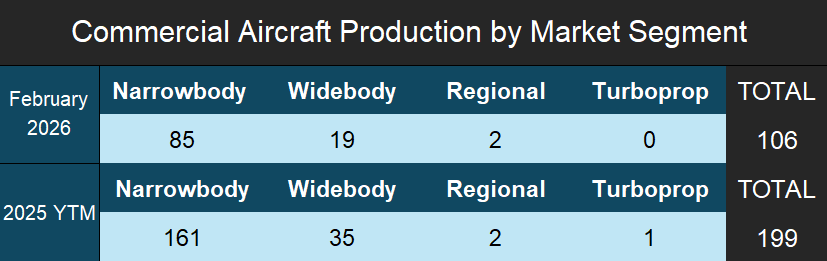

Total commercial aircraft production in February 2026 reached 106 aircraft, marking a clear increase from January and signaling renewed momentum as manufacturers ramp up output early in the year. Production remained heavily concentrated in the narrowbody segment, which accounted for 85 aircraft, while widebody output totaled 19 aircraft, reflecting steady twin-aisle activity. Regional jet production reached two aircraft during the month, and no turboprops were recorded, leaving the overall mix overwhelmingly weighted toward single-aisle platforms.

On a year-to-date basis, total commercial aircraft production reached 199 aircraft through the first two months of 2026. Narrowbodies continue to dominate cumulative output at 161 aircraft, while widebody production stands at 35 aircraft year to date. Regional jet production totals two aircraft, and turboprop output remains minimal at just one aircraft year to date, highlighting relatively quiet activity in the smaller aircraft segments compared with the stronger pace in the narrowbody and widebody categories.

- Production data represents the actual number of aircraft produced in January 2026. Forecast International considers an aircraft produced upon its first flight. This may differ from an OEM’s definition of produced.

Average Production-to-Delivery Lead Times

Average production-to-delivery lead times shortened in February compared to January for both narrowbody and widebody aircraft, reflecting improving alignment between first flight events and deliveries as production volumes increased and major programs continue to ramp up and accelerate into the year. Narrowbody aircraft averaged 22 days from production to delivery, while widebodies averaged 26 days, indicating a more efficient early-year delivery cadence as OEMs build operational momentum. Turboprop lead times averaged 124 days; however, this figure is based on a single data point and should be interpreted as such. No regional jet lead-time data was recorded during the month due to a lack of paired production and delivery events, and both turboprop and regional aircraft production activity have remained notably quiet through the first two months of the year. Across all segments, the weighted average lead time stood at 57 days.

Projected Deliveries

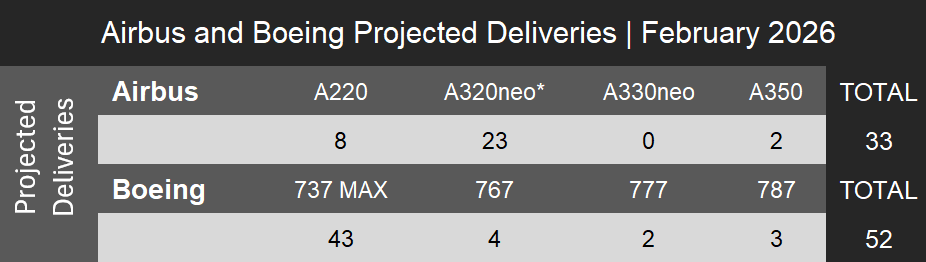

Forecast International estimates that Airbus and Boeing combined delivered approximately 85 aircraft in February 2026. Airbus delivered an estimated 33 aircraft, led by 23 A320neo-family narrowbodies and eight A220s, with widebody activity limited to two A350s and no A330neo deliveries recorded. Deliveries were notably weak for Airbus during the month, primarily due to subdued A320neo-family deliveries, and the performance showed little meaningful improvement compared with January levels. Boeing delivered an estimated 52 aircraft during the month, anchored by 43 737 MAX aircraft, while widebody deliveries included four 767s, two 777s, and three 787s, indicating steady twin-aisle output as the company continues to rebuild delivery stability early in the year.

Notes:

- Delivery data is the expected number that Boeing and Airbus will report in their January 2026 Orders and Deliveries summary and is based on Forecast International’s internal research. Numbers are not official and are not provided by Airbus or Boeing.

- A320neo numbers include all variants for the family; A319neo, A320neo and A321neo

To get a more detailed, month‑by‑month breakdown of commercial aircraft OEM activity, including production, orders, and delivery execution risk, visit https://figlobalintelligence.com/commercial-aircraft-oem-intelligence-brief/

With diverse experience in the commercial aviation industry, Grant joins Forecast International as the Lead Analyst for Commercial Aerospace. He began his career at the Boeing Company, where he worked as a geospatial analyst, designing and building aeronautical navigation charts for Department of Defense flight operations.

Grant then joined a boutique global aviation consulting firm that focused on the aviation finance and leasing industry. In this role he conducted valuations and market analysis of commercial aircraft and engines for banks, private equity firms, lessors and airlines for the purposes of trading, collateralizing and securitizing commercial aviation assets.

Grant has a deep passion for the aviation industry and is also a pilot. He holds his Commercial Pilots License and Instrument Rating in addition to being a FAA Certified Flight Instructor.