Though highly sensitive to macroeconomic trends, production of narrowbody aircraft such as the 737 MAX and A320neo Family are shaped by more complex factors, including air travel demand, supply chain stability, fuel prices, and emerging technologies. U.S. airlines recently cut their revenue and earnings forecasts due to weakening air travel demand amid economic uncertainty and tariffs. Just months ago carriers were expanding capacity and reporting record revenues, but these challenges have since dampened that optimism. Historically, recessions have occurred roughly every decade and given the current outlook, another downturn is now even more likely in the short term. While the impact of a recession on narrowbody aircraft deliveries may vary, analyzing past trends and the current state of commercial aviation offers valuable insight into how the next slowdown could affect deliveries of the A320neo Family and 737 MAX.

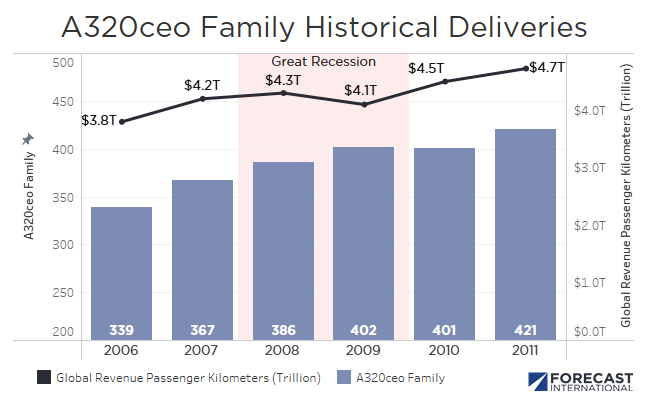

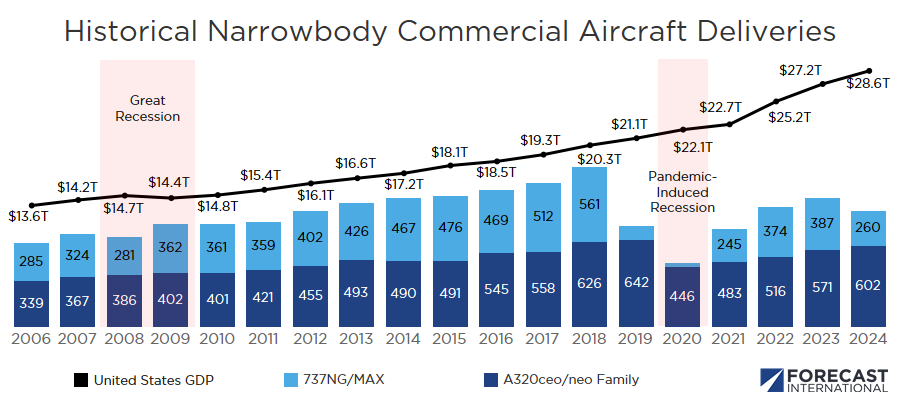

During the global financial crisis, deliveries of A320ceo family and 737NG aircraft declined only slightly from a total of 691 aircraft in 2007 to 667 in 2008—or by 3.47%, representing a total of 24 aircraft. Despite the severity of the economic downturn, deliveries rebounded, surpassing the 691 deliveries seen in 2007 with a total of 764 in 2009 and 762 in 2010. The slight drop in production from 2007 to 2008 was primarily due to a decline in 737NG deliveries, whereas Airbus A320ceo family deliveries actually increased each year from 2006 to 2009 and never declined during this period, even amid the most severe economic downturn since the Great Depression.

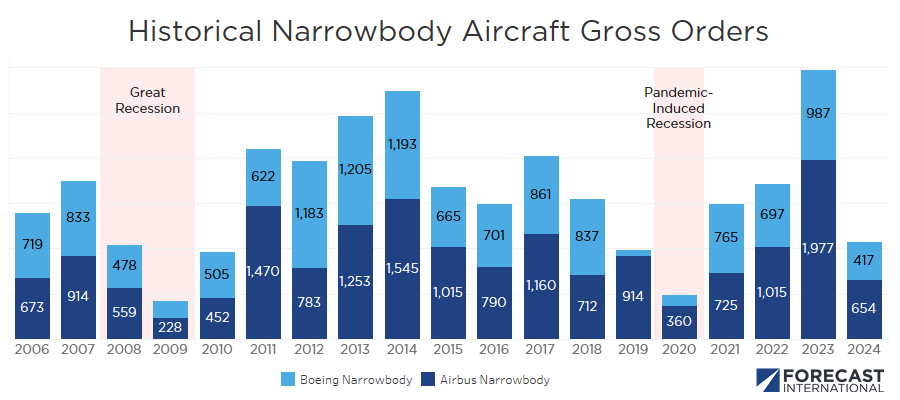

This trend highlights a key reality: during downturns, operators are more likely to retire older, less fuel-efficient aircraft than to cancel orders for new ones, which can be costly—especially if demand rebounds faster than expected. Operators also have the option to defer orders, while OEMs can adjust delivery slots. This dynamic was evident during the COVID-19 pandemic when aircraft orders initially plummeted but later surged to record-breaking levels in 2023 as domestic travel demand exceeded pre-pandemic levels. At the onset of the pandemic, many operators planned to retire a significant number of older aircraft. However, when travel demand recovered quicker than anticipated, airlines scrambled to source 737NG and A320ceo Family aircraft to meet capacity needs and delayed planned retirements to offset delivery delays of 737 MAX and A320neo Family aircraft.

Post-pandemic trends in narrowbody aircraft production and deliveries further highlight the complex factors influencing commercial aircraft manufacturing. Production levels in 2019 were already significantly lower than in previous years due to the 737 MAX grounding. Even now, they have yet to recover to pre-pandemic levels due to persistent supply chain constraints despite record-high air travel demand, strong economic growth, and the need for new-technology narrowbody aircraft in the period following the pandemic. As a result, the primary impact of an economic downturn is typically seen in new aircraft orders rather than deliveries, which declined significantly during both the pandemic and the global financial crisis. Deliveries, on the other hand, can remain relatively stable due to long lead times and contractual commitments, whereas order activity is much more sensitive to economic uncertainty. However, when a cyclical downturn results in a rapid drop in air travel demand, deliveries can decrease significantly, such as during the COVID-19 pandemic or after 9/11.

Given these factors, Forecast International does not anticipate a significant decline in A320neo Family or 737 MAX aircraft deliveries during the next economic downturn, provided it does not involve a severe and sudden collapse in air travel, as seen during the pandemic. In such a scenario, airlines and lessors are more likely to defer orders temporarily, leading to lower delivery rates.

Our expectation of a minimal impact on narrowbody aircraft deliveries in a typical downturn also reflects the current state of the commercial aerospace industry. Ongoing supply chain constraints, historically low production levels of narrowbody aircraft in recent years and sustained high demand for the A320neo family and 737 MAX suggest that an economic downturn could even help rebalance supply chains. This, in turn, might allow production lines to maintain or even modestly increase output as the industry recovers and returns to pre-pandemic production rates. However, we do expect that new aircraft orders will decline significantly during a downturn, as operators prioritize fleet optimization and adjust their existing order books with OEMs. That said, the impact of each downturn varies, and it remains possible that narrowbody aircraft deliveries could decline depending on the nature and severity of the downturn.

With diverse experience in the commercial aviation industry, Grant joins Forecast International as the Lead Analyst for Commercial Aerospace. He began his career at the Boeing Company, where he worked as a geospatial analyst, designing and building aeronautical navigation charts for Department of Defense flight operations.

Grant then joined a boutique global aviation consulting firm that focused on the aviation finance and leasing industry. In this role he conducted valuations and market analysis of commercial aircraft and engines for banks, private equity firms, lessors and airlines for the purposes of trading, collateralizing and securitizing commercial aviation assets.

Grant has a deep passion for the aviation industry and is also a pilot. He holds his Commercial Pilots License and Instrument Rating in addition to being a FAA Certified Flight Instructor.