Boeing Orders Stay Soft as Airbus Wins on Both Narrowbodies and Widebodies // Airbus Slightly Outpaces Boeing Deliveries

August 2025 Summary

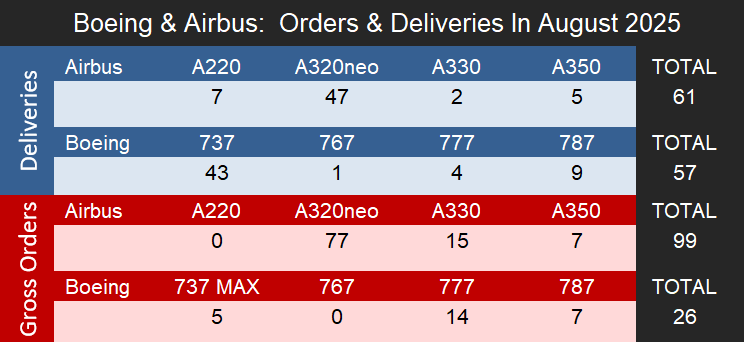

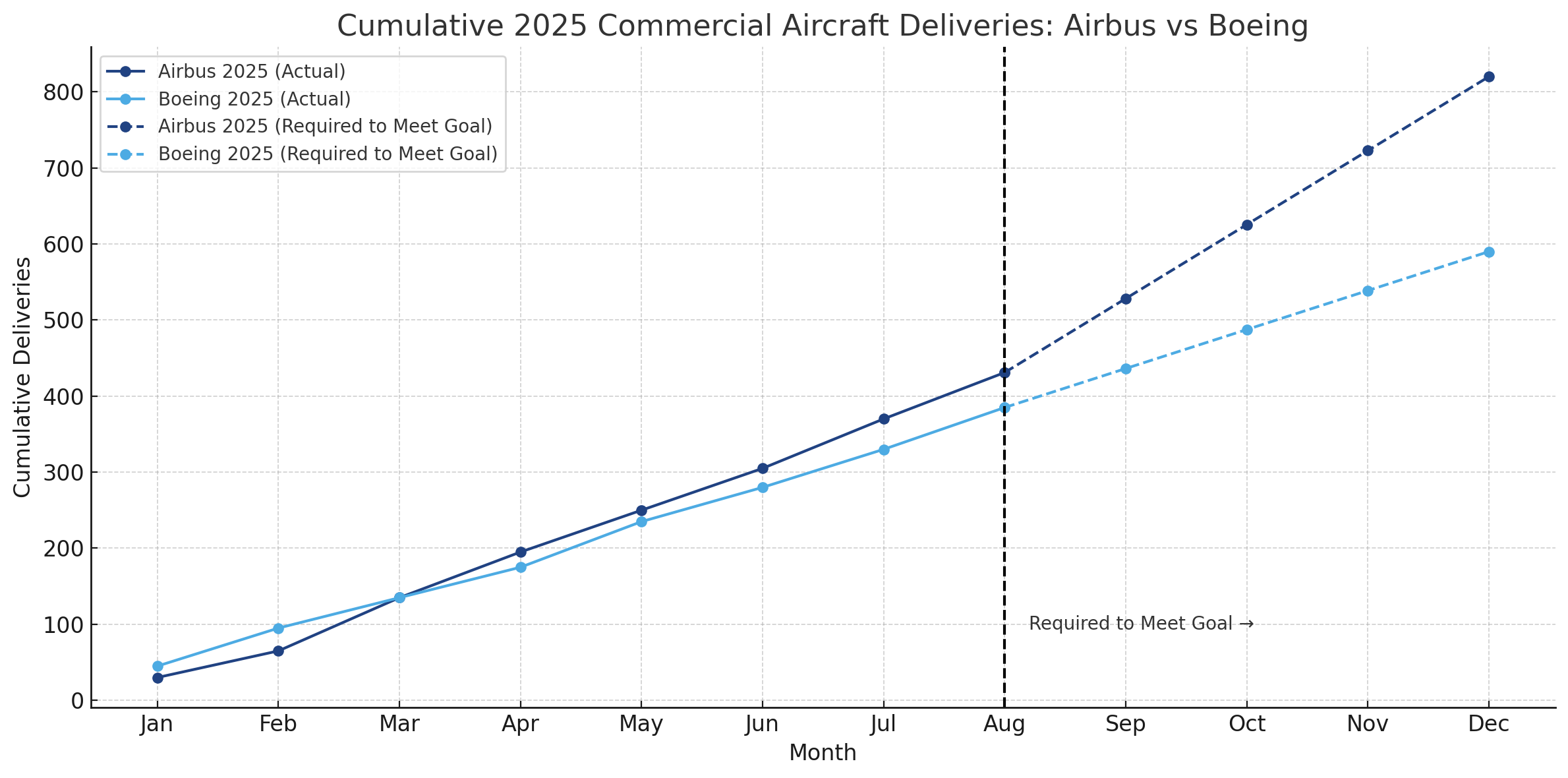

In August, Boeing saw an increase in deliveries compared to July, handing over 57 aircraft (14 widebodies and 43 narrowbodies), while Airbus delivered a total of 61 aircraft (7 widebodies and 54 narrowbodies), below its current estimated production rate target of 67 aircraft per month. Airbus now needs an average of 97 deliveries per month to meet its 2025 delivery target of 820 aircraft. This is a considerable increase from the average of 54 aircraft it delivered in the first eight months of the year, but Airbus has historically shown it can ramp up production in the final months to meet its target. In contrast, Boeing has not set a formal delivery target for 2025 as it continues to focus on quality and stabilizing production across its commercial aircraft programs.

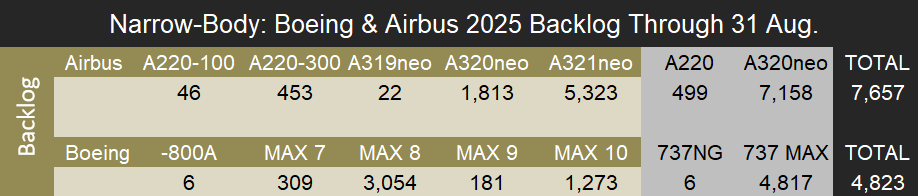

- A320neo numbers include all variants for the family; A319neo, A320neo and A321neo.

Deliveries

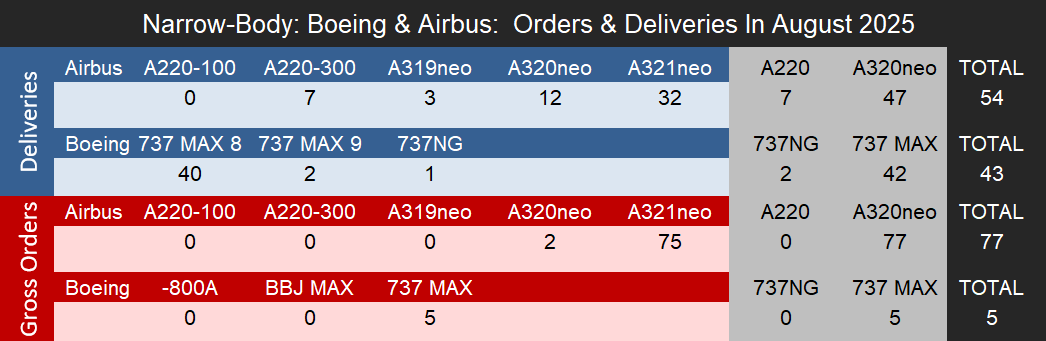

The 57 Boeing jets delivered in August included 42 737 MAXs, one 737-700, one 767-2C, four 777s, and nine 787s. Though Boeing has not released an official delivery target for the year, Forecast International expects around 580 deliveries from the OEM in 2025. Having delivered 385 aircraft through August 31st, Boeing needs to average 49 deliveries per month for the rest of the year to reach a total of 580, a feasible goal considering the manufacturer has already averaged 48 deliveries per month through August 31st. Stabilized MAX production at 38 per month and the continued delivery of remaining MAX and 787 inventory through the end of the year will support this delivery number.

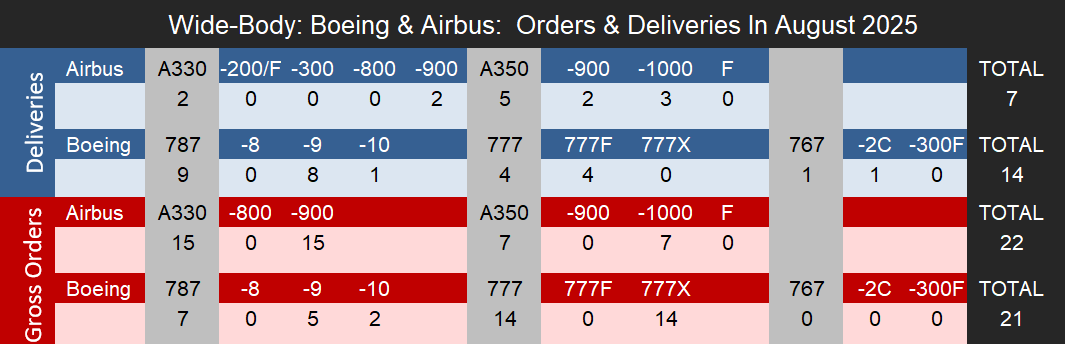

As for its widebody programs, Boeing delivered 54 787s from January 1 through August 31 and a total of nine 787s in the month of August. 787 deliveries are benefiting from increased production rates nearing seven aircraft per month in addition to the drawing down of the remaining 787 inventory by year end. Forecast International believes it will be likely Boeing is able to stabilize the 787 program at seven aircraft per month by year end, making room for a production rate increase to 10 aircraft per month throughout 2026.

Meanwhile, Boeing has delivered a total of 26 777s through August, or an average of around three aircraft per month, in line with the manufacturer’s production target rate of three 777s per month. Additionally, the first 777X delivery is still scheduled for 2026 to Lufthansa as the aircraft inches closer to certification after years of delays. The program recently received a key green light from the FAA to begin Phase 2D of its Type Inspection Authorization (TIA) testing, which focuses on community noise, with Phase 3 evaluations to follow. Phase 3 includes testing of the aircraft’s APU in addition to its stability and control.

In August, Airbus delivered 61 aircraft, including seven A220s, 47 from the A320neo family, two A330s, and five A350s. Ambitious production increases have not yet materialized this year, with some programs like the A350 and A320neo families failing to meet their initial 2025 production targets. However, Airbus has a track record of rapidly increasing production in the final months to meet its delivery goals. Forecast International still believes it is possible for Airbus to reach its target of 820 deliveries for the year, though it is becoming increasingly difficult. A strong September, with at least 75 to 80 deliveries, will be crucial to support the final push toward the goal.

In August, Airbus delivered seven A220s, all of which were A220-300s. Forecast International considers A220 production to be stabilized around eight aircraft per month, though deliveries have oscillated throughout the year, ranging from as few as five to as many as twelve in a single month. This production stability is a positive sign for the program, as it opens the door for future rate increases and more consistent deliveries. We expect production rate increases to continue, though we remain highly doubtful that the target of 14 aircraft per month will be reached by 2026, a goal Airbus had originally planned to achieve.

On the widebody side, Airbus delivered five A350s in August, bringing total 2025 deliveries to just 32 aircraft as of August 31, an average of four aircraft per month, well below the manufacturer’s targeted production rate of six per month. Forecast International continues to view the A350 program as currently struggling from a production and deliveries standpoint. Airbus’ plans to increase output to ten aircraft per month by 2026 remain unrealistic, and we believe the manufacturer will need to focus on stabilizing production and deliveries at around six per month for the remainder of the year before attempting to ramp up further.

Orders

In August, Boeing recorded 26 gross orders, including five for the 737 MAX, seven for the 787, and 14 for the 777X. The 14-aircraft 777X order came from Cathay Pacific for 777-9s. With a total of 35 777Xs on order, the airline is now expected to be the largest 777X operator in the Asia-Pacific region. Year-to-date, Boeing has also outpaced Airbus in gross orders, receiving a total of 725 through August 31st compared to 600 for Airbus, a performance supported by continued demand for MAX aircraft and a significant surge in 787 orders.

Meanwhile, Airbus saw a pickup in orders in August with a total of 99 gross orders, a sharp increase from the seven received in July. The bulk of these orders came from a large deal with aircraft leasing firm Avolon, which placed an order for 75 A320neo aircraft and 15 A330neos.

- For consistency, this article does not include Boeing’s ASC 606 accounting adjustments and considers net orders as gross orders minus cancellations.

Backlog

- Airbus backlog numbers do not include A320ceo or A330-200 ghost orders.

- Boeing backlog numbers do not include 737-700, 737-800 or 777-300ER ghost orders.

- A320neo numbers include all variants for the family; A319neo, A320neo and A321neo

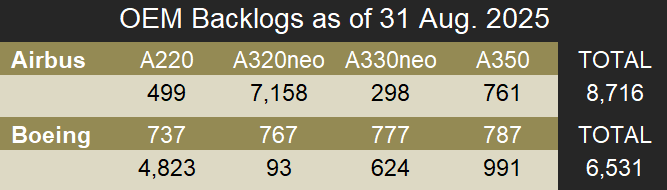

As of August 31, 2025, Airbus reported a backlog of 8,716 jets, excluding the A320ceo and A330-200. Of this backlog, 7,657, or 87.8 percent, consisted of A220 and A320neo narrowbodies. Meanwhile, Boeing’s total unfilled orders before ASC 606 adjustments stood at 6,531 aircraft. Excluding the 737-700, 737-800, and 777-300ER, 4,823, or 73.8 percent, were 737 MAXs. Airbus’s backlog represents 10.6 years of production based on Forecast International’s 2025 production estimates, while Boeing’s backlog would last approximately 11.5 years.

With diverse experience in the commercial aviation industry, Grant joins Forecast International as the Lead Analyst for Commercial Aerospace. He began his career at the Boeing Company, where he worked as a geospatial analyst, designing and building aeronautical navigation charts for Department of Defense flight operations.

Grant then joined a boutique global aviation consulting firm that focused on the aviation finance and leasing industry. In this role he conducted valuations and market analysis of commercial aircraft and engines for banks, private equity firms, lessors and airlines for the purposes of trading, collateralizing and securitizing commercial aviation assets.

Grant has a deep passion for the aviation industry and is also a pilot. He holds his Commercial Pilots License and Instrument Rating in addition to being a FAA Certified Flight Instructor.